Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Quantinuum is filing for a $20 billion IPO, check out everything from the Helios hardware breakthrough to strategic Nvidia partnerships.

On January 14, 2026, Honeywell finally confirmed what a lot of us in the quantum space have been waiting for: Quantinuum has officially filed a confidential draft registration (Form S-1) for its IPO. It is a massive move, not just because it is the most anticipated pure-play quantum listing in years, but because of the price tag being floated. Rumors from those close to the process suggest a valuation target of $20 billion or more. For context, that would double the $10 billion valuation they hit just four months ago during a funding round led by Nvidia and JPMorgan Chase.

To understand why Quantinuum is commanding such a premium, you have to look at its DNA. The company was formed in 2021 by merging Honeywell Quantum Solutions (the hardware muscle) with Cambridge Quantum (the software brains). Unlike some competitors that focus only on the chips, Quantinuum is what we call a “full-stack” provider. They build the computers, the operating systems, and the industry-specific applications.

Honeywell still holds a majority stake of about 54 percent in the venture. By taking it public, Honeywell is essentially “unlocking” the value that has been tucked away inside their massive industrial conglomerate. It also gives Quantinuum the independent capital it needs to keep up with the insane R&D costs of this industry.

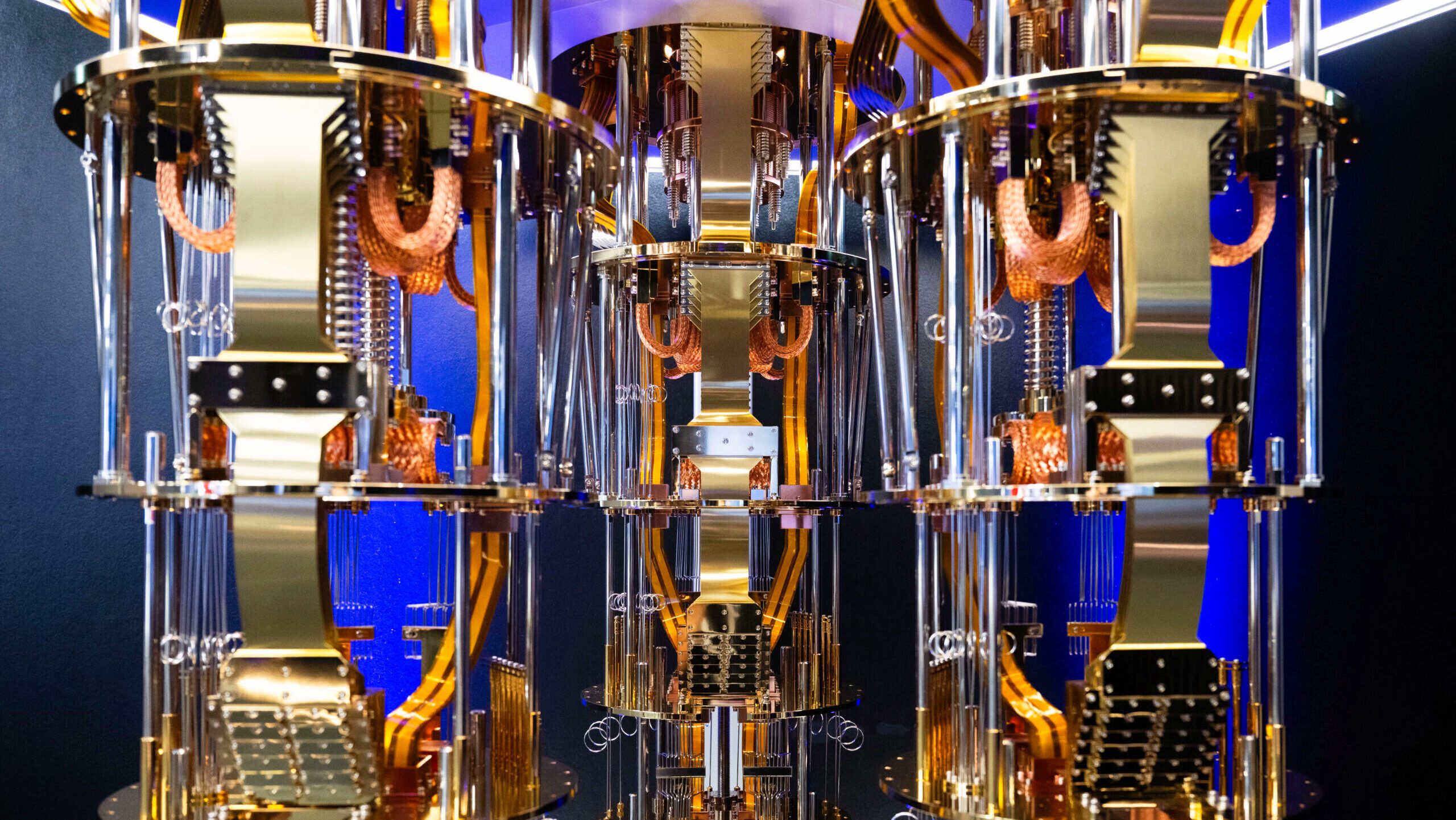

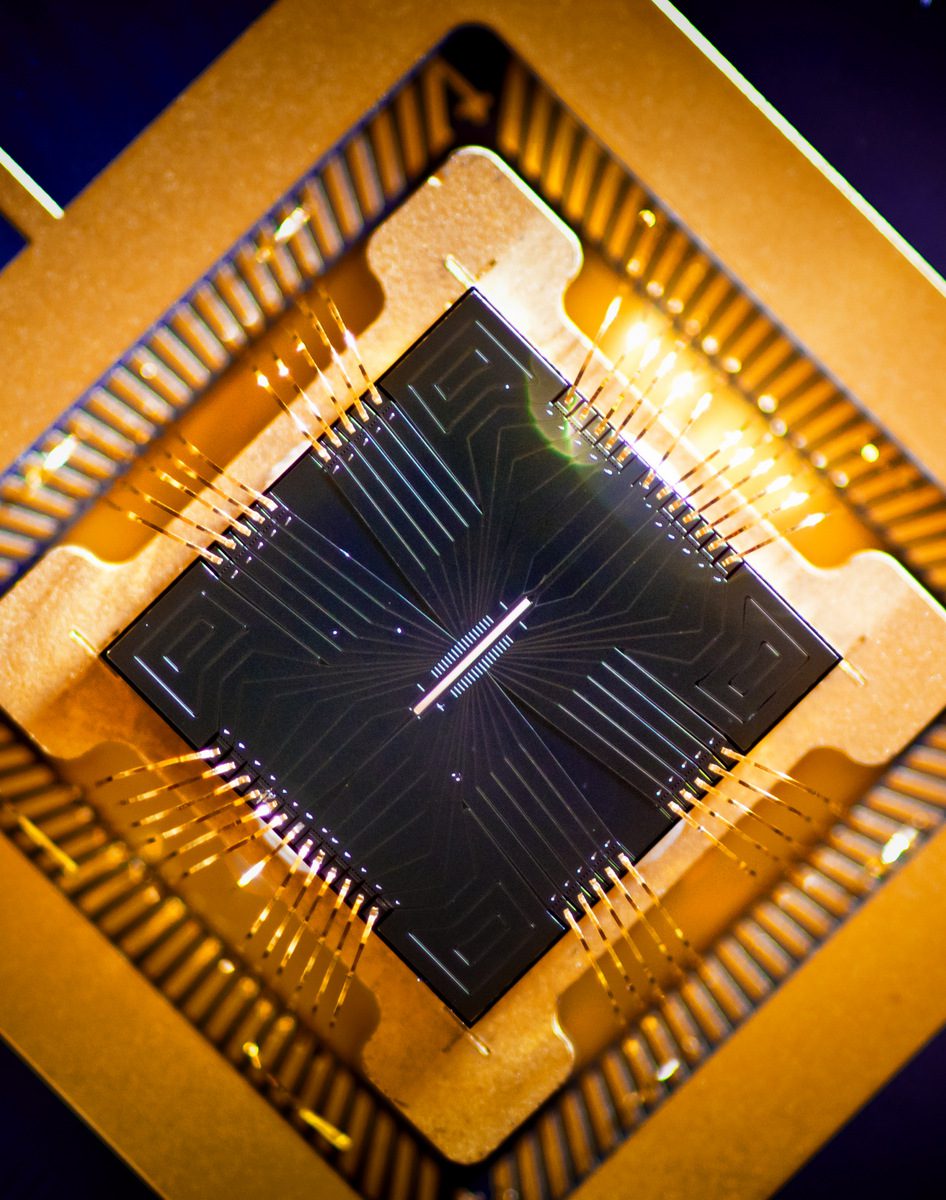

In late 2025, the company launched its Helios system, and the specs are honestly hard to wrap your head around. Helios uses a trapped-ion architecture, specifically a Quantum Charge-Coupled Device (QCCD) design. Instead of fixed qubits on a silicon chip like you would see from IBM or Google, Quantinuum uses individual barium-137 ions that they physically shuttle through a trap.

The big win for Helios is that it achieved “better than break-even” performance with 50 logical qubits. In the quantum world, “noisy” physical qubits are prone to errors, so you bundle them together into logical qubits that can correct themselves. Helios hit a single-qubit gate fidelity of 99.9975 percent, which is the highest reported for any commercial system. This accuracy allows for all-to-all connectivity, meaning any qubit can talk to any other qubit without having to “hop” through neighbors.

While the hardware gets the headlines, the software side is arguably more “ready” for the real world. Quantinuum has two main pillars here:

They have already signed up a “who’s who” of enterprise partners including BMW for battery research, Airbus for materials science, and HSBC for financial modeling. Their partnership with Nvidia is particularly interesting because they are using Nvidia Grace Hopper GPUs to handle the heavy lifting of real-time error decoding.

If we look at the numbers, things get a bit more “speculative.” According to Honeywell’s recent segment reporting, Quantinuum (which sits in their “Corporate and All Other” bucket) reported roughly $24 million in revenue through the first nine months of 2025.

At a $20 billion valuation, we are looking at a Price-to-Sales (P/S) ratio that makes even the wildest SaaS companies look cheap. However, look at the other pure-plays on the market:

Quantinuum is entering the market as the largest player by cap, but with revenue that is actually lower than IonQ. The market is clearly betting on the technical superiority of the trapped-ion approach and the safety net of Honeywell’s industrial backing.

Confidential filings mean we won’t see the full S-1 for a few months. Most analysts are eyeing a listing date in late 2026. The big catalyst to watch in the meantime will be the DARPA Quantum Benchmarking Initiative. Quantinuum is currently in Stage B. If they can get independent validation that their hardware can solve real-world problems that classical supercomputers cannot touch, that $20 billion target might actually start to look reasonable.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

Quantinuum is filing for a $20 billion IPO, check out everything from the Helios hardware breakthrough to strategic Nvidia partnerships.

On January 14, 2026, Honeywell finally confirmed what a lot of us in the quantum space have been waiting for: Quantinuum has officially filed a confidential draft registration (Form S-1) for its IPO. It is a massive move, not just because it is the most anticipated pure-play quantum listing in years, but because of the price tag being floated. Rumors from those close to the process suggest a valuation target of $20 billion or more. For context, that would double the $10 billion valuation they hit just four months ago during a funding round led by Nvidia and JPMorgan Chase.

To understand why Quantinuum is commanding such a premium, you have to look at its DNA. The company was formed in 2021 by merging Honeywell Quantum Solutions (the hardware muscle) with Cambridge Quantum (the software brains). Unlike some competitors that focus only on the chips, Quantinuum is what we call a “full-stack” provider. They build the computers, the operating systems, and the industry-specific applications.

Honeywell still holds a majority stake of about 54 percent in the venture. By taking it public, Honeywell is essentially “unlocking” the value that has been tucked away inside their massive industrial conglomerate. It also gives Quantinuum the independent capital it needs to keep up with the insane R&D costs of this industry.

In late 2025, the company launched its Helios system, and the specs are honestly hard to wrap your head around. Helios uses a trapped-ion architecture, specifically a Quantum Charge-Coupled Device (QCCD) design. Instead of fixed qubits on a silicon chip like you would see from IBM or Google, Quantinuum uses individual barium-137 ions that they physically shuttle through a trap.

The big win for Helios is that it achieved “better than break-even” performance with 50 logical qubits. In the quantum world, “noisy” physical qubits are prone to errors, so you bundle them together into logical qubits that can correct themselves. Helios hit a single-qubit gate fidelity of 99.9975 percent, which is the highest reported for any commercial system. This accuracy allows for all-to-all connectivity, meaning any qubit can talk to any other qubit without having to “hop” through neighbors.

While the hardware gets the headlines, the software side is arguably more “ready” for the real world. Quantinuum has two main pillars here:

They have already signed up a “who’s who” of enterprise partners including BMW for battery research, Airbus for materials science, and HSBC for financial modeling. Their partnership with Nvidia is particularly interesting because they are using Nvidia Grace Hopper GPUs to handle the heavy lifting of real-time error decoding.

If we look at the numbers, things get a bit more “speculative.” According to Honeywell’s recent segment reporting, Quantinuum (which sits in their “Corporate and All Other” bucket) reported roughly $24 million in revenue through the first nine months of 2025.

At a $20 billion valuation, we are looking at a Price-to-Sales (P/S) ratio that makes even the wildest SaaS companies look cheap. However, look at the other pure-plays on the market:

Quantinuum is entering the market as the largest player by cap, but with revenue that is actually lower than IonQ. The market is clearly betting on the technical superiority of the trapped-ion approach and the safety net of Honeywell’s industrial backing.

Confidential filings mean we won’t see the full S-1 for a few months. Most analysts are eyeing a listing date in late 2026. The big catalyst to watch in the meantime will be the DARPA Quantum Benchmarking Initiative. Quantinuum is currently in Stage B. If they can get independent validation that their hardware can solve real-world problems that classical supercomputers cannot touch, that $20 billion target might actually start to look reasonable.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.