Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

IonQ acquires SkyWater for $1.8 billion, creating the first vertically integrated quantum platform to accelerate fault-tolerant computing and secure US supply.

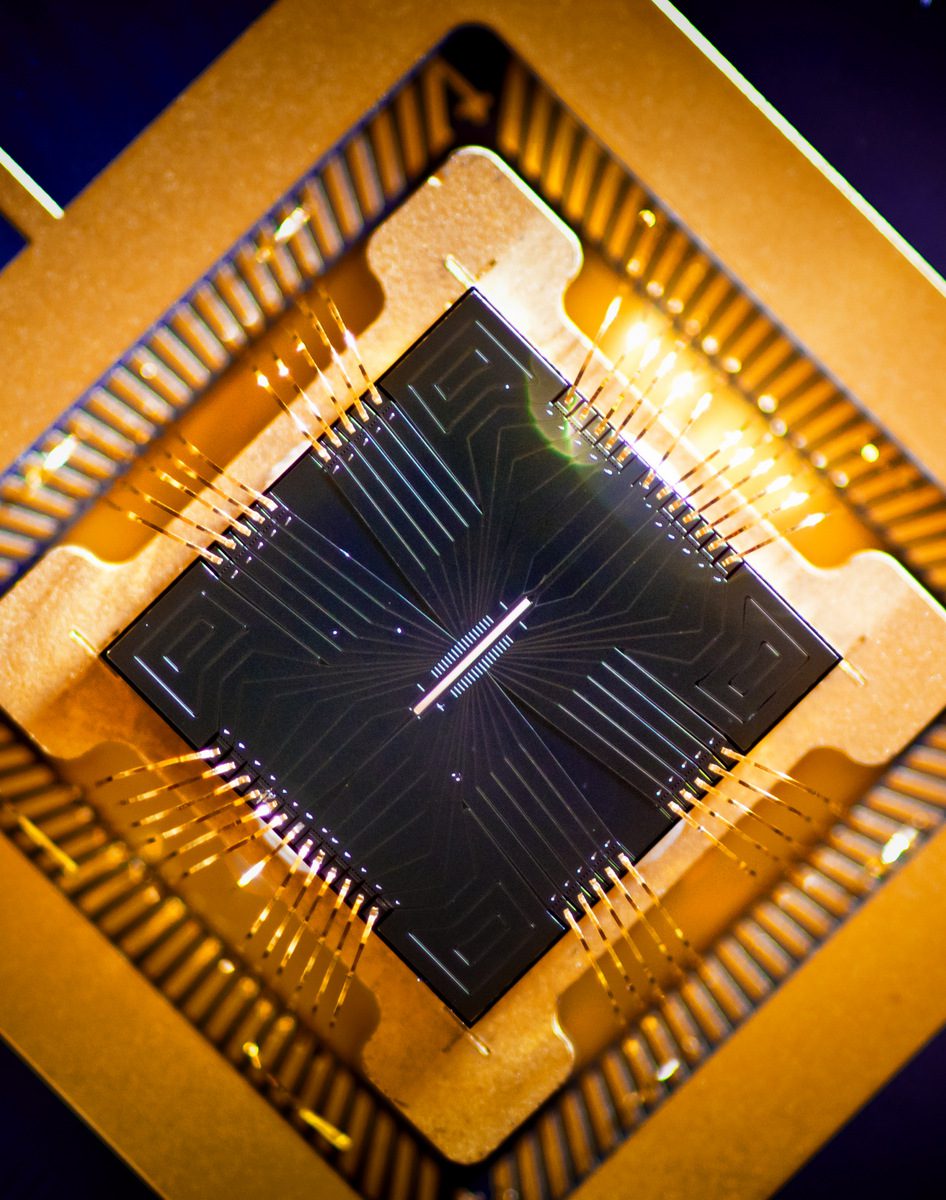

The landscape of high-performance computing shifted fundamentally on January 26, 2026, when IonQ (NYSE: IONQ) announced its definitive agreement to acquire SkyWater Technology (NASDAQ: SKYT). In a deal valued at approximately $1.8 billion, IonQ is not just buying a partner: it is buying the means of production. This move represents the first time a quantum computing leader has moved to fully vertically integrate its supply chain by absorbing a commercial semiconductor foundry.

For years, the “fabless” model was the standard for quantum startups, where designs were sent to external giants for fabrication. By bringing SkyWater’s domestic, trusted foundry capabilities in-house, IonQ is attempting to solve the industry’s most persistent bottleneck: the slow and expensive iteration cycle of quantum chip development. This analysis explores the strategic “why” behind this merger, the financial mechanics of the $1.8 billion transaction, and what it means for the sovereign compute landscape in 2026.

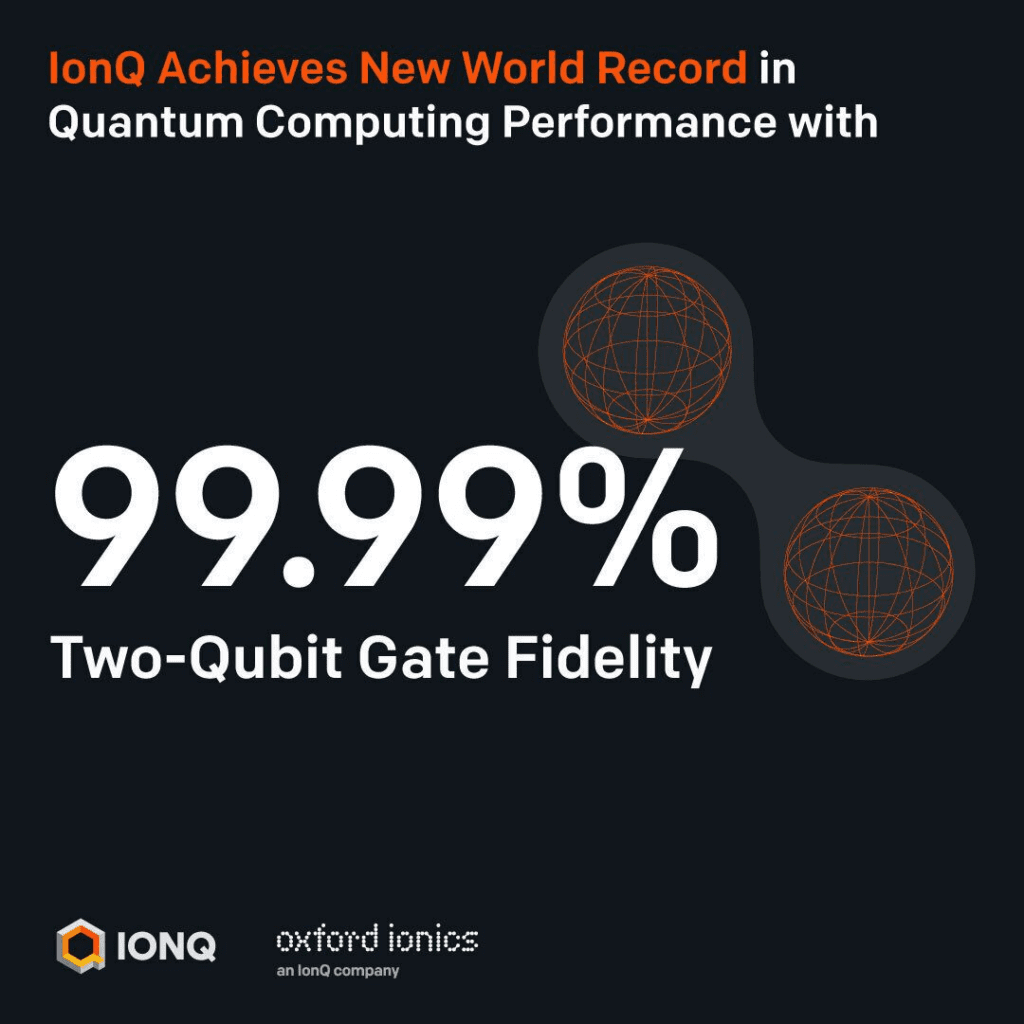

IonQ enters this transaction as a dominant force in the trapped-ion quantum modality. Throughout 2025, the company hit a series of technical milestones that separated it from the speculative pack. It achieved its Algorithmic Qubit (AQ) 64 goal three months ahead of schedule and demonstrated a world-record 99.99% two-qubit gate fidelity. These metrics are critical because they represent the threshold for practical, fault-tolerant quantum computing.

SkyWater Technology, based in Bloomington, Minnesota, serves as the largest exclusively U.S.-based pure-play semiconductor foundry. It operates under a unique “Technology as a Service” (TaaS) model, which focuses on co-creating emerging technologies rather than just churning out commodity chips. SkyWater is a DMEA-accredited Category 1A Trusted Foundry, a designation that makes it an essential partner for the U.S. Department of Defense and other national security agencies.

The merger combines IonQ’s leading quantum architecture with SkyWater’s established manufacturing footprint in Minnesota, Florida, and Texas. Post-close, SkyWater will operate as a wholly owned subsidiary, maintaining its own name and continuing to serve its broad base of existing customers in AI, aerospace, and healthcare.

The context of this deal is a global race for “quantum sovereignty.” As quantum computing moves from laboratory experiments to national security infrastructure, the ability to manufacture hardware domestically has become a strategic priority.

The acquisition also follows IonQ’s late-2025 purchase of Oxford Ionics, which brought in critical “ion-trap-on-a-chip” technology. While the UK government has required those operations to remain anchored in Britain for national security reasons, the SkyWater deal allows IonQ to “port” those designs to a U.S. production line for domestic defense contracts.

The combined entity creates a unique dual-track revenue model. On one side is IonQ’s high-growth “Quantum-as-a-Service” (QCaaS) and on the other is SkyWater’s established foundry revenue.

IonQ generates revenue primarily through access to its quantum computers via major cloud providers like AWS and Azure, as well as direct government and enterprise partnerships.

SkyWater brings a more traditional, yet specialized, revenue stream based on its TaaS model.

The financial mechanics of the acquisition are designed to provide SkyWater shareholders with a significant premium while maintaining IonQ’s long-term liquidity.

IonQ enters 2026 with a “war chest” that is unprecedented in the quantum sector. Following a $2.0 billion equity offering in October 2025, the company’s pro-forma cash balance rose to approximately $3.5 billion. This massive liquidity allows IonQ to fund the $1.8 billion acquisition while still maintaining roughly $2.5 billion in cash to execute its hardware roadmap.

In tandem with the merger news, IonQ announced that it expects its full-year 2025 revenue results to land at the high end or above its prior guidance of $106 million to $110 million. This sustained growth trajectory has boosted investor confidence, with IonQ stock rising roughly 2% on the news of the acquisition.

The most compelling argument for this merger is the acceleration of IonQ’s technical roadmap. In the semiconductor world, “time to silicon” is the ultimate metric.

By owning the foundry, IonQ can run multiple “generational prototypes” in parallel.

Acquiring a DMEA-accredited Category 1A Trusted Foundry secures IonQ’s position as the primary quantum partner for the U.S. government. This “end-to-end” domestic supply chain—from design and prototyping to manufacturing and packaging—is a major strategic asset in a world where global supply chains are increasingly fragile.

Despite the clear strategic benefits, merging a high-growth, high-loss quantum company with a capital-intensive foundry business is not without significant risk.

The acquisition of SkyWater Technology by IonQ is a landmark event that marks the end of the “experimental” phase of the quantum industry and the beginning of the “industrial” phase. By utilizing its $3.5 billion cash position to buy a trusted foundry, IonQ has fundamentally changed the unit economics and the velocity of quantum hardware development.

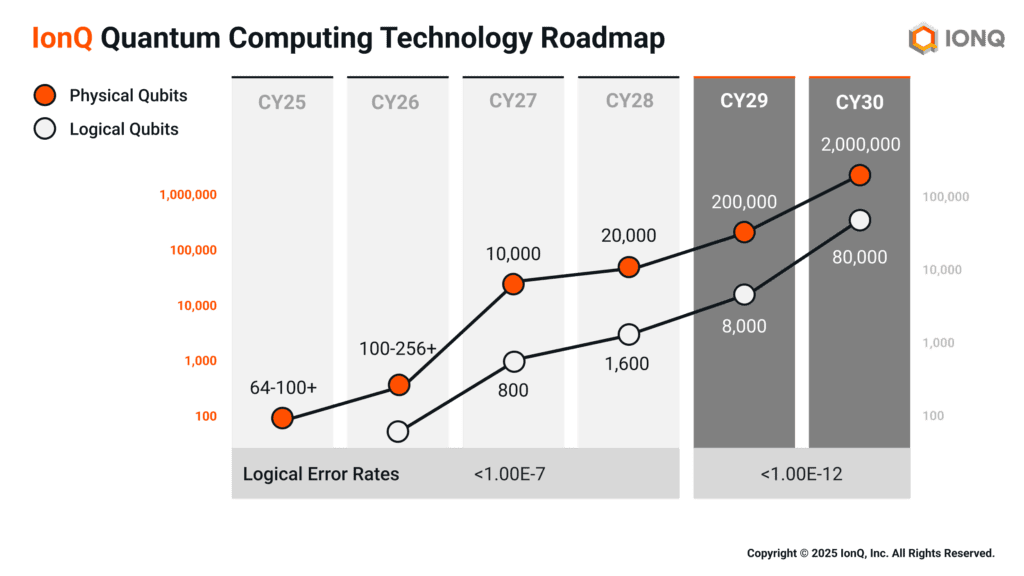

The true success of this merger will be measured by whether IonQ can actually hit its new 2028 target for a 200,000-qubit processor. If vertical integration delivers on its promise of 75% faster cycle times, IonQ may have just secured a lead in the quantum era that no competitor can catch.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

IonQ acquires SkyWater for $1.8 billion, creating the first vertically integrated quantum platform to accelerate fault-tolerant computing and secure US supply.

The landscape of high-performance computing shifted fundamentally on January 26, 2026, when IonQ (NYSE: IONQ) announced its definitive agreement to acquire SkyWater Technology (NASDAQ: SKYT). In a deal valued at approximately $1.8 billion, IonQ is not just buying a partner: it is buying the means of production. This move represents the first time a quantum computing leader has moved to fully vertically integrate its supply chain by absorbing a commercial semiconductor foundry.

For years, the “fabless” model was the standard for quantum startups, where designs were sent to external giants for fabrication. By bringing SkyWater’s domestic, trusted foundry capabilities in-house, IonQ is attempting to solve the industry’s most persistent bottleneck: the slow and expensive iteration cycle of quantum chip development. This analysis explores the strategic “why” behind this merger, the financial mechanics of the $1.8 billion transaction, and what it means for the sovereign compute landscape in 2026.

IonQ enters this transaction as a dominant force in the trapped-ion quantum modality. Throughout 2025, the company hit a series of technical milestones that separated it from the speculative pack. It achieved its Algorithmic Qubit (AQ) 64 goal three months ahead of schedule and demonstrated a world-record 99.99% two-qubit gate fidelity. These metrics are critical because they represent the threshold for practical, fault-tolerant quantum computing.

SkyWater Technology, based in Bloomington, Minnesota, serves as the largest exclusively U.S.-based pure-play semiconductor foundry. It operates under a unique “Technology as a Service” (TaaS) model, which focuses on co-creating emerging technologies rather than just churning out commodity chips. SkyWater is a DMEA-accredited Category 1A Trusted Foundry, a designation that makes it an essential partner for the U.S. Department of Defense and other national security agencies.

The merger combines IonQ’s leading quantum architecture with SkyWater’s established manufacturing footprint in Minnesota, Florida, and Texas. Post-close, SkyWater will operate as a wholly owned subsidiary, maintaining its own name and continuing to serve its broad base of existing customers in AI, aerospace, and healthcare.

The context of this deal is a global race for “quantum sovereignty.” As quantum computing moves from laboratory experiments to national security infrastructure, the ability to manufacture hardware domestically has become a strategic priority.

The acquisition also follows IonQ’s late-2025 purchase of Oxford Ionics, which brought in critical “ion-trap-on-a-chip” technology. While the UK government has required those operations to remain anchored in Britain for national security reasons, the SkyWater deal allows IonQ to “port” those designs to a U.S. production line for domestic defense contracts.

The combined entity creates a unique dual-track revenue model. On one side is IonQ’s high-growth “Quantum-as-a-Service” (QCaaS) and on the other is SkyWater’s established foundry revenue.

IonQ generates revenue primarily through access to its quantum computers via major cloud providers like AWS and Azure, as well as direct government and enterprise partnerships.

SkyWater brings a more traditional, yet specialized, revenue stream based on its TaaS model.

The financial mechanics of the acquisition are designed to provide SkyWater shareholders with a significant premium while maintaining IonQ’s long-term liquidity.

IonQ enters 2026 with a “war chest” that is unprecedented in the quantum sector. Following a $2.0 billion equity offering in October 2025, the company’s pro-forma cash balance rose to approximately $3.5 billion. This massive liquidity allows IonQ to fund the $1.8 billion acquisition while still maintaining roughly $2.5 billion in cash to execute its hardware roadmap.

In tandem with the merger news, IonQ announced that it expects its full-year 2025 revenue results to land at the high end or above its prior guidance of $106 million to $110 million. This sustained growth trajectory has boosted investor confidence, with IonQ stock rising roughly 2% on the news of the acquisition.

The most compelling argument for this merger is the acceleration of IonQ’s technical roadmap. In the semiconductor world, “time to silicon” is the ultimate metric.

By owning the foundry, IonQ can run multiple “generational prototypes” in parallel.

Acquiring a DMEA-accredited Category 1A Trusted Foundry secures IonQ’s position as the primary quantum partner for the U.S. government. This “end-to-end” domestic supply chain—from design and prototyping to manufacturing and packaging—is a major strategic asset in a world where global supply chains are increasingly fragile.

Despite the clear strategic benefits, merging a high-growth, high-loss quantum company with a capital-intensive foundry business is not without significant risk.

The acquisition of SkyWater Technology by IonQ is a landmark event that marks the end of the “experimental” phase of the quantum industry and the beginning of the “industrial” phase. By utilizing its $3.5 billion cash position to buy a trusted foundry, IonQ has fundamentally changed the unit economics and the velocity of quantum hardware development.

The true success of this merger will be measured by whether IonQ can actually hit its new 2028 target for a 200,000-qubit processor. If vertical integration delivers on its promise of 75% faster cycle times, IonQ may have just secured a lead in the quantum era that no competitor can catch.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.