Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Celestica’s record-shattering Q4 2025 results showcase a massive leap in adjusted operating margins to 7.7%, driven by surging demand for AI data center technologies.

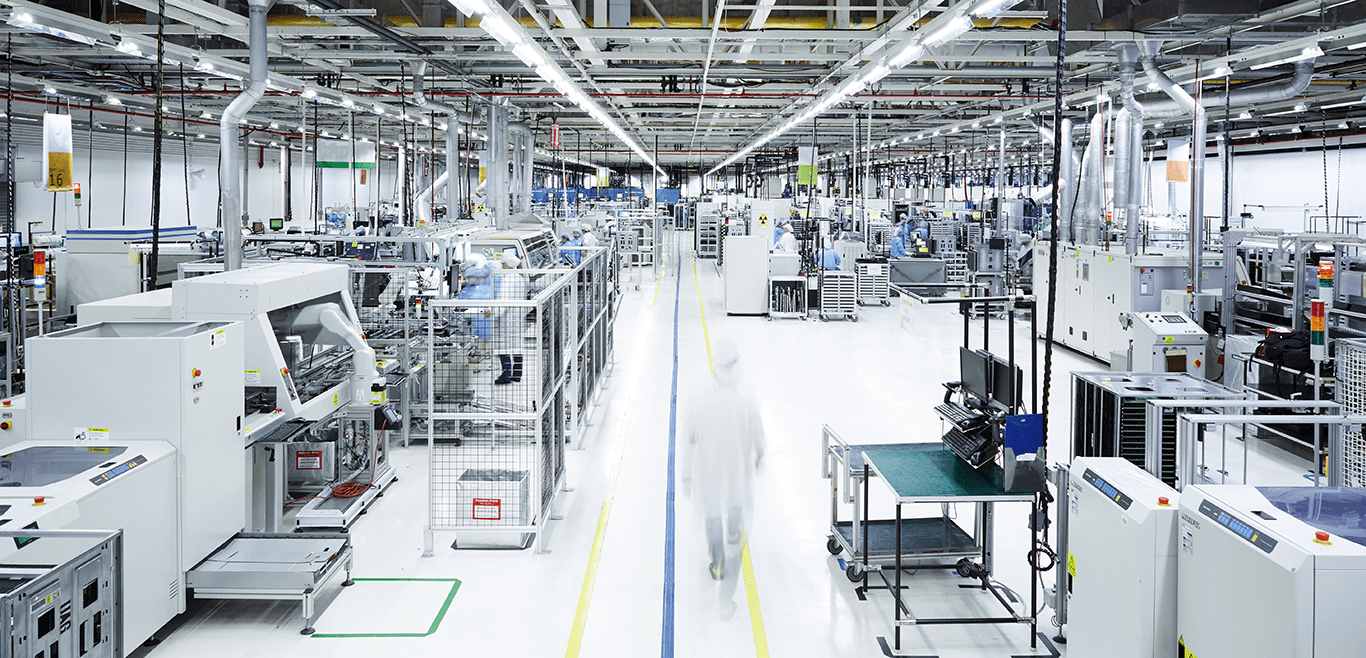

The electronics manufacturing services (EMS) sector was once viewed as a domain of glacial progress, defined by low-margin, high-volume commodity business where success was measured in basis points. For decades, investors treated companies in this space as mere assembly arms with little pricing power or intellectual property. That era is officially over for Celestica (NYSE: CLS). As the company reported its fourth-quarter and full-year 2025 financial results on January 28, 2026, it became clear that Celestica has successfully transcended its legacy roots to become a high-value infrastructure partner for the AI age.

For analysts and potential investors, the primary concern with EMS companies has always been margin thinness. The fear is that these firms are simply pass-through entities for hardware components, bearing the inventory risk with none of the software-like upside. Celestica’s Q4 results have effectively dismantled that thesis. By delivering an adjusted operating margin of 7.7%, the company has not only beat its own guidance but has signaled a structural shift in its earnings power. This is no longer just about assembly: it is about the design, integration, and deployment of the most complex compute fabrics on the planet.

Celestica operates through two primary segments: Connectivity & Cloud Solutions (CCS) and Advanced Technology Solutions (ATS). While the ATS segment handles diversified markets like aerospace, defense, and health tech, the CCS segment has become the company’s rocket ship. Within CCS, the Hardware Platform Solutions (HPS) business is the star. This is where Celestica designs and manufactures the complex switching platforms and AI/ML compute systems that power the world’s largest hyperscale data centers.

The company has pivoted from being a generalist contract manufacturer to a specialist in high-complexity, high-growth technology platforms. They are no longer just “assembling” parts: they are co-developing next-generation AI infrastructure with giants like Google and other hyperscalers. This move up the value chain, focusing on HPS and proprietary design, is the fundamental driver behind the recent financial outperformance.

The headline numbers for Q4 2025 were undeniably impressive: revenue reached $3.65 billion, a 44% increase year-over-year compared to the $2.55 billion reported in Q4 2024. For the serious investor, however, the real story is found in the operating leverage and the aggressive expansion of the bottom line.

The adjusted operating margin reached 7.7% in Q4, compared to 6.8% in the same period last year. This 90-basis-point expansion is massive in the context of global manufacturing, where such gains often take years of incremental efficiency to achieve. This shift was not an accident: it was the result of a deliberate strategy to focus on higher-margin, technology-intensive programs.

This expansion was primarily driven by operating leverage within the CCS segment. As the volume of high-complexity AI hardware increases, Celestica’s fixed costs are spread over a larger revenue base. More importantly, the revenue mix is shifting toward more profitable HPS programs. In Q4, HPS revenue grew by a staggering 72% year-over-year, now representing roughly $1.4 billion of the total pie. When 40% of your business is growing at 70% with higher-than-average margins, the math for margin expansion becomes very compelling.

Management’s decision to align the company’s capital allocation with the AI boom is paying off in real-time. The quarterly report highlighted several key catalysts that explain the current trajectory and suggest that this is the beginning of a multi-year cycle rather than a temporary peak.

One of the most discussed topics in the analyst community has been Celestica’s role in the production of Google’s Tensor Processing Units (TPUs). While rumors of supply chain diversification occasionally weigh on the stock, the reality on the ground is one of deepening partnership. Celestica officially announced an expansion of its manufacturing capacity in the United States to support the production of Google TPU systems.

This expansion, scheduled for completion in 2027, is designed to enhance Celestica’s ability to support the production of complex data center hardware. By being a preferred partner for Google’s custom AI silicon, Celestica has secured a high-barrier-to-entry position in the most critical segment of the data center. Their higher production yields and expertise in rack-level solutions make them difficult to replace, even as hyperscalers naturally seek to diversify their sourcing for risk mitigation.

Networking is often the unsung hero of the AI revolution. Large language models (LLMs) require massive bandwidth to move data between thousands of GPUs with minimal latency. Celestica announced it was awarded a program for a 1.6 terabyte switching platform with its third hyperscaler customer. This award is a significant validator of their HPS roadmap.

The company recently introduced its DS6000 and DS6001 switches, which double the capacity of current 800G offerings. By winning these 1.6T programs today, Celestica is locking in high-margin revenue for 2027 and 2028. This is a classic “moat” strategy: they are moving faster than the legacy networking giants, providing the “open networking” solutions that hyperscalers prefer for their massive clusters.

Perhaps the most bullish signal in the entire report was the massive increase in planned capital investments. Celestica now expects 2026 capital expenditures to reach approximately $1.0 billion, or roughly 6% of revenue. For a company that was once capital-light, this is a bold statement of confidence in the future.

Crucially, CEO Rob Mionis stated that the company expects to fund this expansion organically through operating cash flow. This is a vital point for analysts: Celestica is growing at a massive clip without needing to dilute shareholders or take on excessive debt. The investments will include expanding the manufacturing footprint in the Dallas-Fort Worth area, constructing new buildings at their Thailand campus, and upgrading sites in Mexico and Japan. This global network provides the geographic flexibility and scale that hyperscalers demand for their global AI rollouts.

To understand Celestica’s financial health, one must look at the divergence between its two operating units.

The CCS segment is where the AI “magic” is happening. With revenue of $2.86 billion (up 64% YoY) and a segment margin of 8.4%, this division is the primary driver of both top-line growth and margin expansion.

The ATS segment, while currently less exciting than CCS, provides a diversified base that balances the portfolio. Revenue in Q4 was $0.80 billion, down 1% year-over-year.

The momentum in the AI space has allowed Celestica to significantly raise its 2026 annual outlook, a move that caught many in the market by surprise given the already record-high 2025 performance.

This guidance suggests that the 56% EPS growth seen in 2025 is not a one-time event. Instead, it is the beginning of a multi-year secular trend as AI shifts from training large models to large-scale inference and enterprise deployment.

While the financial results are glowing, no seasoned analyst would ignore the potential headwinds.

The investment case for Celestica has fundamentally changed. They are no longer a “me-too” contract manufacturer fighting for scraps. They have transformed into an “AI Utility”—the essential physical layer that enables the software-defined future.

For analysts concerned about margins, the record 7.7% adjusted operating margin is the definitive proof of concept. The company is successfully leveraging its expertise in 800G/1.6T networking, high-density storage, and custom AI compute to drive structural profitability. With the company now guiding for $8.75 in adjusted EPS for 2026, the valuation remains attractive relative to its earnings growth profile.

Celestica has positioned itself at the nexus of the most significant technology shift in a generation. By investing heavily in capacity today to meet the demand of tomorrow, they are building a moat that will be difficult for competitors to cross. For the long-term investor, Celestica is the essential infrastructure partner for the AI revolution.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

Celestica’s record-shattering Q4 2025 results showcase a massive leap in adjusted operating margins to 7.7%, driven by surging demand for AI data center technologies.

The electronics manufacturing services (EMS) sector was once viewed as a domain of glacial progress, defined by low-margin, high-volume commodity business where success was measured in basis points. For decades, investors treated companies in this space as mere assembly arms with little pricing power or intellectual property. That era is officially over for Celestica (NYSE: CLS). As the company reported its fourth-quarter and full-year 2025 financial results on January 28, 2026, it became clear that Celestica has successfully transcended its legacy roots to become a high-value infrastructure partner for the AI age.

For analysts and potential investors, the primary concern with EMS companies has always been margin thinness. The fear is that these firms are simply pass-through entities for hardware components, bearing the inventory risk with none of the software-like upside. Celestica’s Q4 results have effectively dismantled that thesis. By delivering an adjusted operating margin of 7.7%, the company has not only beat its own guidance but has signaled a structural shift in its earnings power. This is no longer just about assembly: it is about the design, integration, and deployment of the most complex compute fabrics on the planet.

Celestica operates through two primary segments: Connectivity & Cloud Solutions (CCS) and Advanced Technology Solutions (ATS). While the ATS segment handles diversified markets like aerospace, defense, and health tech, the CCS segment has become the company’s rocket ship. Within CCS, the Hardware Platform Solutions (HPS) business is the star. This is where Celestica designs and manufactures the complex switching platforms and AI/ML compute systems that power the world’s largest hyperscale data centers.

The company has pivoted from being a generalist contract manufacturer to a specialist in high-complexity, high-growth technology platforms. They are no longer just “assembling” parts: they are co-developing next-generation AI infrastructure with giants like Google and other hyperscalers. This move up the value chain, focusing on HPS and proprietary design, is the fundamental driver behind the recent financial outperformance.

The headline numbers for Q4 2025 were undeniably impressive: revenue reached $3.65 billion, a 44% increase year-over-year compared to the $2.55 billion reported in Q4 2024. For the serious investor, however, the real story is found in the operating leverage and the aggressive expansion of the bottom line.

The adjusted operating margin reached 7.7% in Q4, compared to 6.8% in the same period last year. This 90-basis-point expansion is massive in the context of global manufacturing, where such gains often take years of incremental efficiency to achieve. This shift was not an accident: it was the result of a deliberate strategy to focus on higher-margin, technology-intensive programs.

This expansion was primarily driven by operating leverage within the CCS segment. As the volume of high-complexity AI hardware increases, Celestica’s fixed costs are spread over a larger revenue base. More importantly, the revenue mix is shifting toward more profitable HPS programs. In Q4, HPS revenue grew by a staggering 72% year-over-year, now representing roughly $1.4 billion of the total pie. When 40% of your business is growing at 70% with higher-than-average margins, the math for margin expansion becomes very compelling.

Management’s decision to align the company’s capital allocation with the AI boom is paying off in real-time. The quarterly report highlighted several key catalysts that explain the current trajectory and suggest that this is the beginning of a multi-year cycle rather than a temporary peak.

One of the most discussed topics in the analyst community has been Celestica’s role in the production of Google’s Tensor Processing Units (TPUs). While rumors of supply chain diversification occasionally weigh on the stock, the reality on the ground is one of deepening partnership. Celestica officially announced an expansion of its manufacturing capacity in the United States to support the production of Google TPU systems.

This expansion, scheduled for completion in 2027, is designed to enhance Celestica’s ability to support the production of complex data center hardware. By being a preferred partner for Google’s custom AI silicon, Celestica has secured a high-barrier-to-entry position in the most critical segment of the data center. Their higher production yields and expertise in rack-level solutions make them difficult to replace, even as hyperscalers naturally seek to diversify their sourcing for risk mitigation.

Networking is often the unsung hero of the AI revolution. Large language models (LLMs) require massive bandwidth to move data between thousands of GPUs with minimal latency. Celestica announced it was awarded a program for a 1.6 terabyte switching platform with its third hyperscaler customer. This award is a significant validator of their HPS roadmap.

The company recently introduced its DS6000 and DS6001 switches, which double the capacity of current 800G offerings. By winning these 1.6T programs today, Celestica is locking in high-margin revenue for 2027 and 2028. This is a classic “moat” strategy: they are moving faster than the legacy networking giants, providing the “open networking” solutions that hyperscalers prefer for their massive clusters.

Perhaps the most bullish signal in the entire report was the massive increase in planned capital investments. Celestica now expects 2026 capital expenditures to reach approximately $1.0 billion, or roughly 6% of revenue. For a company that was once capital-light, this is a bold statement of confidence in the future.

Crucially, CEO Rob Mionis stated that the company expects to fund this expansion organically through operating cash flow. This is a vital point for analysts: Celestica is growing at a massive clip without needing to dilute shareholders or take on excessive debt. The investments will include expanding the manufacturing footprint in the Dallas-Fort Worth area, constructing new buildings at their Thailand campus, and upgrading sites in Mexico and Japan. This global network provides the geographic flexibility and scale that hyperscalers demand for their global AI rollouts.

To understand Celestica’s financial health, one must look at the divergence between its two operating units.

The CCS segment is where the AI “magic” is happening. With revenue of $2.86 billion (up 64% YoY) and a segment margin of 8.4%, this division is the primary driver of both top-line growth and margin expansion.

The ATS segment, while currently less exciting than CCS, provides a diversified base that balances the portfolio. Revenue in Q4 was $0.80 billion, down 1% year-over-year.

The momentum in the AI space has allowed Celestica to significantly raise its 2026 annual outlook, a move that caught many in the market by surprise given the already record-high 2025 performance.

This guidance suggests that the 56% EPS growth seen in 2025 is not a one-time event. Instead, it is the beginning of a multi-year secular trend as AI shifts from training large models to large-scale inference and enterprise deployment.

While the financial results are glowing, no seasoned analyst would ignore the potential headwinds.

The investment case for Celestica has fundamentally changed. They are no longer a “me-too” contract manufacturer fighting for scraps. They have transformed into an “AI Utility”—the essential physical layer that enables the software-defined future.

For analysts concerned about margins, the record 7.7% adjusted operating margin is the definitive proof of concept. The company is successfully leveraging its expertise in 800G/1.6T networking, high-density storage, and custom AI compute to drive structural profitability. With the company now guiding for $8.75 in adjusted EPS for 2026, the valuation remains attractive relative to its earnings growth profile.

Celestica has positioned itself at the nexus of the most significant technology shift in a generation. By investing heavily in capacity today to meet the demand of tomorrow, they are building a moat that will be difficult for competitors to cross. For the long-term investor, Celestica is the essential infrastructure partner for the AI revolution.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.