Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

SanDisk reports a blowout Q2 2026 with $3.03 billion in revenue and $6.20 EPS. Despite the stock being down today, the future valuation remains massive.

The landscape of the global memory market has shifted from a period of severe oversupply to a strategic gold rush. For SanDisk (NASDAQ: SNDK), which completed its spinoff from Western Digital in February 2025, the latest fiscal second-quarter results ending January 2, 2026, serve as a definitive proof of concept for the pure-play flash strategy. As I sat with my coffee this morning looking at the results, it was clear that SanDisk is no longer just a consumer brand: it has become a critical pillar of the AI infrastructure layer.

You might be looking at the red on your screen today and wondering what happened. Despite a quarter that can only be described as a blowout, the stock is trading down roughly 4% in the early session. This is a classic “sell the news” reaction after a year where SanDisk was one of the top performers in the semiconductor space. For the disciplined analyst, however, this noise is secondary to the signal: the numbers behind the curtain are fundamentally altering the company’s valuation profile.

For analysts and potential investors, the primary concern has historically been the cyclicality of NAND flash pricing. The fear was that memory remained a commodity business where margins are crushed during every downturn. SanDisk’s Q2 results have challenged this narrative. By delivering a non-GAAP gross margin of 51.1% and a sequential revenue jump of 31%, the company has demonstrated that specialized, high-performance storage for AI is commanding a premium that transcends the traditional commodity cycle.

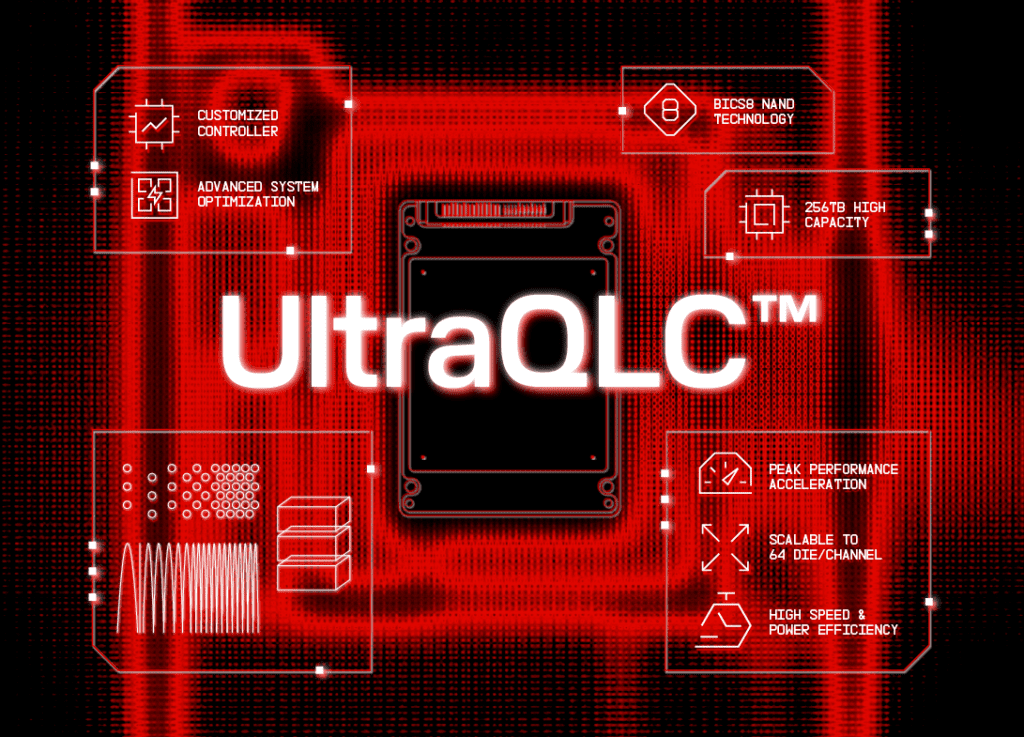

SanDisk operates as a focused leader in non-volatile memory (NAND) and solid-state drives (SSDs). Following its separation from Western Digital’s hard drive business, management has pivoted aggressively toward high-performance datacenter solutions and Edge AI computing. The company’s core advantage lies in its joint venture with Kioxia, which provides a massive, cost-efficient manufacturing base: and its BiCS technology roadmap, which is currently transitioning to high-density BiCS8 architectures.

The spinoff was a gamble on focus. While Western Digital kept the legacy HDD business, SanDisk was freed to chase the more volatile, but higher-growth, flash market. Management’s bet was that by removing the drag of the slower HDD segment, they could attract a higher valuation multiple more aligned with pure-play semiconductor firms.

The company has successfully moved up the value chain. Instead of competing solely on price-per-gigabyte in the consumer market, SanDisk is now co-developing “Stargate” storage class products for hyperscalers. This shift from retail memory cards to enterprise-grade SSDs is the primary engine behind the current margin expansion. When you look at the supply chain, SanDisk is essentially moving from being a component maker to a strategic design partner for the world’s largest data centers.

The headline numbers for the fiscal second quarter were nothing short of a blowout compared to Street expectations. Revenue reached $3.03 billion, comfortably beating the high end of management’s own $2.65 billion guidance.

The most striking figure in the report was the non-GAAP gross margin, which expanded to 51.1%, up from 29.9% in the prior quarter. This is a massive 2,120-basis-point sequential jump that reflects a perfect storm of better product mix and sharp price increases in the enterprise SSD market.

| Metric | Q2 2026 Actual | Q1 2026 (Prior) | Q2 2025 (YoY) |

|---|---|---|---|

| Revenue | $3.03 Billion | $2.31 Billion | $1.88 Billion |

| Non-GAAP Gross Margin | 51.1% | 29.9% | 32.5% |

| Operating Income | $1.13 Billion | $245 Million | $233 Million |

| Adjusted EPS | $6.20 | $1.22 | $1.23 |

The financial story is one of aggressive operating leverage. While revenue grew 31% sequentially, operating income surged by 362%. This disconnect highlights how SanDisk’s structural reset, which involves aligning supply with high-value demand, has allowed them to capture nearly every incremental dollar of revenue as profit. It is a level of efficiency we rarely see in the hardware space: it suggests that SanDisk has finally broken the back of the boom-bust cycle that has plagued memory investors for decades.

Management’s decision to prioritize disciplined growth over market share at all costs is yielding record results. Several key catalysts from the latest quarter explain the trajectory.

Datacenter revenue was the standout performer, growing 64% sequentially to $440 million. This was fueled by the rapid adoption of high-performance enterprise SSDs by AI infrastructure builders. As AI models move from training to inference, the need for fast, reliable data access has made SanDisk’s PCIe Gen5 drives essential.

CEO David Goeckeler noted that datacenter is expected to become the largest market for NAND in 2026. SanDisk is capitalizing on this by shifting capacity away from lower-margin consumer products toward these high-density enterprise solutions. In simple terms: they are selling more “expensive” bits to customers who are less price-sensitive because their alternative is leaving billion-dollar AI clusters sitting idle.

SanDisk is currently qualifying its BiCS8 QLC (Quad-Level Cell) storage class product, codenamed “Stargate,” with two major hyperscalers. These drives are designed specifically for the massive data ingestion requirements of AI workloads. By utilizing QLC technology, SanDisk can provide the density needed for AI at scale while maintaining a lower cost structure than traditional TLC (Triple-Level Cell) drives.

The Stargate architecture is particularly impressive because it tackles the bottleneck of “write endurance” in QLC. Traditionally, QLC was seen as too fragile for enterprise use, but SanDisk’s controller technology has bridged that gap. This technical edge is expected to provide a significant revenue tailwind in the second half of 2026 as these qualifications move into volume production.

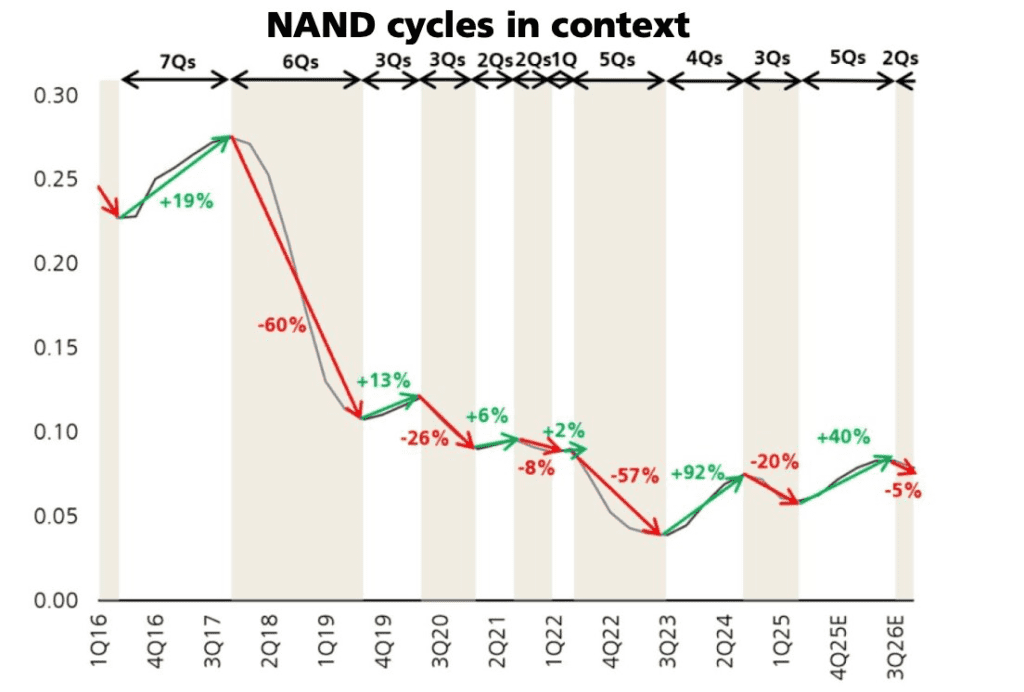

The memory industry has finally learned from its past mistakes. Rather than flooding the market with bits to win a few points of market share, SanDisk and its peers have maintained strict capital expenditure discipline. SanDisk’s bit shipments grew only in the low single digits during the quarter, yet revenue climbed 31%.

This implies that the vast majority of the growth was driven by a mid-30% increase in average selling prices (ASPs). For investors, this is the ideal scenario: profit growth driven by pricing power rather than capital-intensive volume expansion. It indicates a level of maturity in the industry that has been absent for a generation.

The forward outlook provided by management was so strong it actually seemed to confuse the market, contributing to today’s volatile price action. When a company triples the consensus estimate for the upcoming quarter, investors often look for the “catch.”

If we annualize that $13 mid-point EPS, we are looking at $52 in annual earnings power. At today’s share price, which has dipped on the “sell the news” sentiment, SanDisk is trading at a forward P/E ratio that is in the low single digits. Even if you assume that NAND pricing cools off in late 2026, the current valuation is essentially pricing in a total collapse of the market: a scenario that seems unlikely given the current AI infrastructure build-out.

The P/S (Price-to-Sales) ratio also tells a story of undervaluation. While high-flying AI chipmakers trade at 20x or 30x sales, SanDisk is trading at a fraction of that, despite being the “gasoline” that powers the AI engine. As the market begins to realize that high-performance storage is just as essential as the GPU, we expect to see a significant “multiple rerating” for SanDisk.

Despite the overwhelming success of the latest quarter, SanDisk faces several high-class problems:

The investment case for SanDisk has evolved from a cyclical recovery play to a structural AI powerhouse. By securing its own manufacturing through the Kioxia JV and focusing on the high-margin enterprise SSD market, SanDisk has created a moat based on technical performance and supply chain security.

For analysts focused on margins, the jump to over 50% gross margin is the definitive signal. SanDisk has successfully decoupled from the low-margin retail market and positioned itself at the center of the AI-driven data economy. While the stock is red today, the fundamentals suggest that this is a “digestion phase” for a stock that has fundamentally moved its goalposts. With a forward outlook that triples consensus earnings estimates, SanDisk is no longer just a memory company: it is a core beneficiary of the most significant compute shift in a generation.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

SanDisk reports a blowout Q2 2026 with $3.03 billion in revenue and $6.20 EPS. Despite the stock being down today, the future valuation remains massive.

The landscape of the global memory market has shifted from a period of severe oversupply to a strategic gold rush. For SanDisk (NASDAQ: SNDK), which completed its spinoff from Western Digital in February 2025, the latest fiscal second-quarter results ending January 2, 2026, serve as a definitive proof of concept for the pure-play flash strategy. As I sat with my coffee this morning looking at the results, it was clear that SanDisk is no longer just a consumer brand: it has become a critical pillar of the AI infrastructure layer.

You might be looking at the red on your screen today and wondering what happened. Despite a quarter that can only be described as a blowout, the stock is trading down roughly 4% in the early session. This is a classic “sell the news” reaction after a year where SanDisk was one of the top performers in the semiconductor space. For the disciplined analyst, however, this noise is secondary to the signal: the numbers behind the curtain are fundamentally altering the company’s valuation profile.

For analysts and potential investors, the primary concern has historically been the cyclicality of NAND flash pricing. The fear was that memory remained a commodity business where margins are crushed during every downturn. SanDisk’s Q2 results have challenged this narrative. By delivering a non-GAAP gross margin of 51.1% and a sequential revenue jump of 31%, the company has demonstrated that specialized, high-performance storage for AI is commanding a premium that transcends the traditional commodity cycle.

SanDisk operates as a focused leader in non-volatile memory (NAND) and solid-state drives (SSDs). Following its separation from Western Digital’s hard drive business, management has pivoted aggressively toward high-performance datacenter solutions and Edge AI computing. The company’s core advantage lies in its joint venture with Kioxia, which provides a massive, cost-efficient manufacturing base: and its BiCS technology roadmap, which is currently transitioning to high-density BiCS8 architectures.

The spinoff was a gamble on focus. While Western Digital kept the legacy HDD business, SanDisk was freed to chase the more volatile, but higher-growth, flash market. Management’s bet was that by removing the drag of the slower HDD segment, they could attract a higher valuation multiple more aligned with pure-play semiconductor firms.

The company has successfully moved up the value chain. Instead of competing solely on price-per-gigabyte in the consumer market, SanDisk is now co-developing “Stargate” storage class products for hyperscalers. This shift from retail memory cards to enterprise-grade SSDs is the primary engine behind the current margin expansion. When you look at the supply chain, SanDisk is essentially moving from being a component maker to a strategic design partner for the world’s largest data centers.

The headline numbers for the fiscal second quarter were nothing short of a blowout compared to Street expectations. Revenue reached $3.03 billion, comfortably beating the high end of management’s own $2.65 billion guidance.

The most striking figure in the report was the non-GAAP gross margin, which expanded to 51.1%, up from 29.9% in the prior quarter. This is a massive 2,120-basis-point sequential jump that reflects a perfect storm of better product mix and sharp price increases in the enterprise SSD market.

| Metric | Q2 2026 Actual | Q1 2026 (Prior) | Q2 2025 (YoY) |

|---|---|---|---|

| Revenue | $3.03 Billion | $2.31 Billion | $1.88 Billion |

| Non-GAAP Gross Margin | 51.1% | 29.9% | 32.5% |

| Operating Income | $1.13 Billion | $245 Million | $233 Million |

| Adjusted EPS | $6.20 | $1.22 | $1.23 |

The financial story is one of aggressive operating leverage. While revenue grew 31% sequentially, operating income surged by 362%. This disconnect highlights how SanDisk’s structural reset, which involves aligning supply with high-value demand, has allowed them to capture nearly every incremental dollar of revenue as profit. It is a level of efficiency we rarely see in the hardware space: it suggests that SanDisk has finally broken the back of the boom-bust cycle that has plagued memory investors for decades.

Management’s decision to prioritize disciplined growth over market share at all costs is yielding record results. Several key catalysts from the latest quarter explain the trajectory.

Datacenter revenue was the standout performer, growing 64% sequentially to $440 million. This was fueled by the rapid adoption of high-performance enterprise SSDs by AI infrastructure builders. As AI models move from training to inference, the need for fast, reliable data access has made SanDisk’s PCIe Gen5 drives essential.

CEO David Goeckeler noted that datacenter is expected to become the largest market for NAND in 2026. SanDisk is capitalizing on this by shifting capacity away from lower-margin consumer products toward these high-density enterprise solutions. In simple terms: they are selling more “expensive” bits to customers who are less price-sensitive because their alternative is leaving billion-dollar AI clusters sitting idle.

SanDisk is currently qualifying its BiCS8 QLC (Quad-Level Cell) storage class product, codenamed “Stargate,” with two major hyperscalers. These drives are designed specifically for the massive data ingestion requirements of AI workloads. By utilizing QLC technology, SanDisk can provide the density needed for AI at scale while maintaining a lower cost structure than traditional TLC (Triple-Level Cell) drives.

The Stargate architecture is particularly impressive because it tackles the bottleneck of “write endurance” in QLC. Traditionally, QLC was seen as too fragile for enterprise use, but SanDisk’s controller technology has bridged that gap. This technical edge is expected to provide a significant revenue tailwind in the second half of 2026 as these qualifications move into volume production.

The memory industry has finally learned from its past mistakes. Rather than flooding the market with bits to win a few points of market share, SanDisk and its peers have maintained strict capital expenditure discipline. SanDisk’s bit shipments grew only in the low single digits during the quarter, yet revenue climbed 31%.

This implies that the vast majority of the growth was driven by a mid-30% increase in average selling prices (ASPs). For investors, this is the ideal scenario: profit growth driven by pricing power rather than capital-intensive volume expansion. It indicates a level of maturity in the industry that has been absent for a generation.

The forward outlook provided by management was so strong it actually seemed to confuse the market, contributing to today’s volatile price action. When a company triples the consensus estimate for the upcoming quarter, investors often look for the “catch.”

If we annualize that $13 mid-point EPS, we are looking at $52 in annual earnings power. At today’s share price, which has dipped on the “sell the news” sentiment, SanDisk is trading at a forward P/E ratio that is in the low single digits. Even if you assume that NAND pricing cools off in late 2026, the current valuation is essentially pricing in a total collapse of the market: a scenario that seems unlikely given the current AI infrastructure build-out.

The P/S (Price-to-Sales) ratio also tells a story of undervaluation. While high-flying AI chipmakers trade at 20x or 30x sales, SanDisk is trading at a fraction of that, despite being the “gasoline” that powers the AI engine. As the market begins to realize that high-performance storage is just as essential as the GPU, we expect to see a significant “multiple rerating” for SanDisk.

Despite the overwhelming success of the latest quarter, SanDisk faces several high-class problems:

The investment case for SanDisk has evolved from a cyclical recovery play to a structural AI powerhouse. By securing its own manufacturing through the Kioxia JV and focusing on the high-margin enterprise SSD market, SanDisk has created a moat based on technical performance and supply chain security.

For analysts focused on margins, the jump to over 50% gross margin is the definitive signal. SanDisk has successfully decoupled from the low-margin retail market and positioned itself at the center of the AI-driven data economy. While the stock is red today, the fundamentals suggest that this is a “digestion phase” for a stock that has fundamentally moved its goalposts. With a forward outlook that triples consensus earnings estimates, SanDisk is no longer just a memory company: it is a core beneficiary of the most significant compute shift in a generation.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.