Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.

Today’s market is as convoluted as it gets — year to date the S&P 500 is up just 1.46%, essentially the fourth time we’ve reached that mark in just three months. Software stocks have seen their valuations absolutely obliterated, while AI companies have seen their stock prices follow suit. Who knows what each day brings for the market? And that’s without including every single policy change and political interaction that each wild, wild day includes.

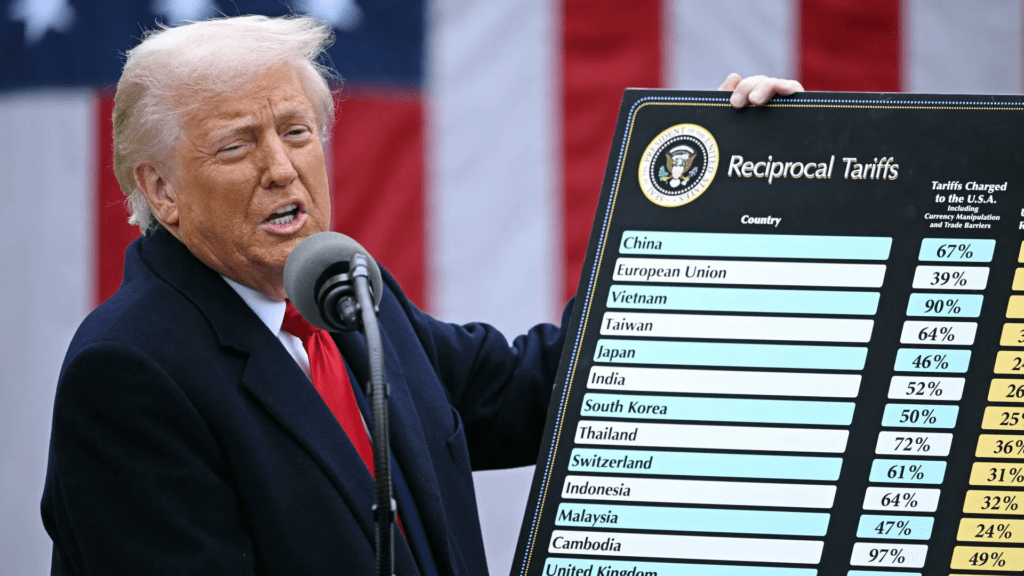

Speaking of, that’s how we started off the year, Trump’s tariffs bringing huge swings in stock pricing and market moves. Some days stocks shot up 10%, before getting absolutely obliterated the next day. Policy uncertainty in Washington pushes stocks lower while promises of trillions in tariff revenue boosts markets the next day. Nobody knows just how tariffs might be implemented or impact global trade, and it seems nobody really cares to determine anything concrete or resolute, when we can rely on the chaos of the standard 2026 day.

The good news comes for those that love buying the dip though — this uncertainty has dragged down the valuation of the S&P 500, despite record numbers from the index’s top companies, from 22x price to earnings at the start of the year down to a more manageable 20 times, much more in line with previous and historical figures. While many valuations for individual stocks are inflated (obviously), the overall index and market as a whole have tended to found a much softer landing for valuations. PEG (price to earnings/earnings growth ratio) figures have fallen, with many of the top companies (including the multi-trillion-dollar NVIDIA) having fallen below a 1X ratio, a figure famously touted as suggesting affordability in stocks compared to their earnings potential.

Nonetheless, Wall Street doesn’t seem to be very optimistic about the chances for the market to continue this substantial growth, discounting stocks relative to their recent valuations off worries of slower growth and general tariff headwinds. It seems much of the recent broad market pullback has been because of worries over valuation, meaning that we’re reaching much more affordable positions despite growth that has continued above expectations. While Wall Street keeps cutting growth forecasts for many of the larger, AI-focused corporations, it seems that each company brings a new surprise in quarterly earnings or their projected upcoming reports for the positive.

Despite this cut, much of the disappointment in earnings have actually come from defensive positions. Home improvement stalwarts Lowe’s and Home Depot reported earnings this week, Lowe’s actually beating on both top-line and bottom-line growth (and reporting nearly 10% growth year over year!), before being dragged down on soft growth expectations for the next year. While AI companies and many software corporations have begun to actually re-up their projections for their 2026 reports, many defensive opportunities have seen slower growth or worries about the general environment.

Even with these issues though, defensive positions have held up better than hypergrowth stocks — capital keeps rotating from these riskier investments into small-caps, industries, and the like despite disappointing earnings and concerns over a softer spending market and slowed non-AI GDP growth. Doesn’t seem to impact the money being invested though.

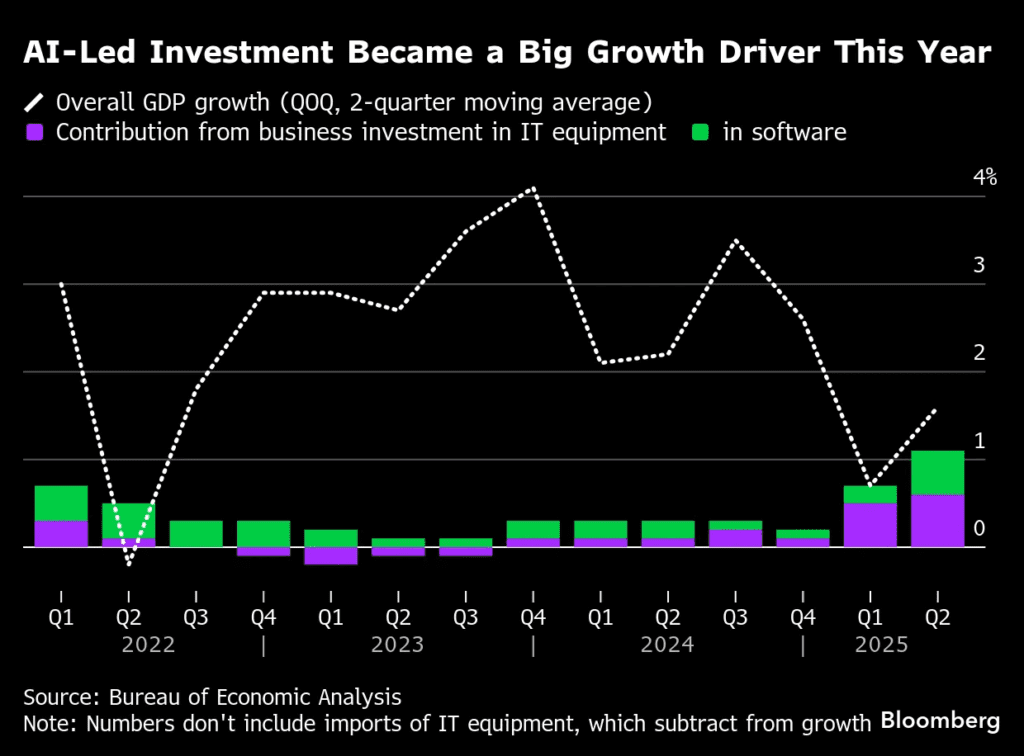

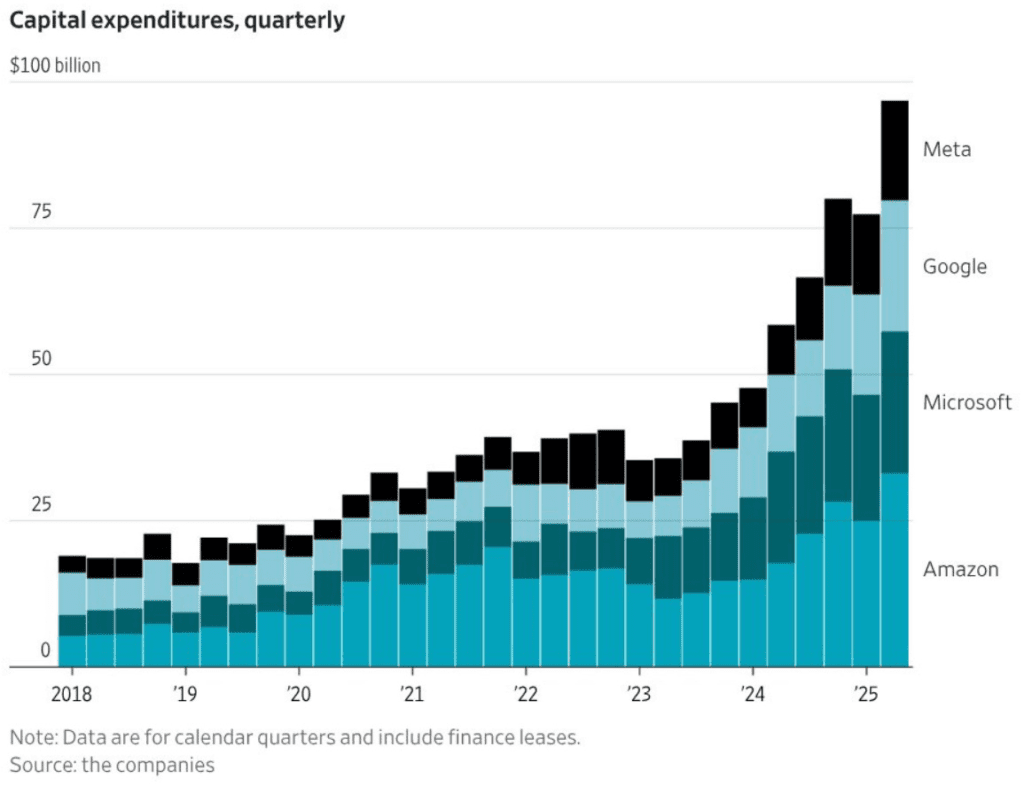

Speaking of AI GDP growth, back to the subject at hand — yes, tech sector valuations are STILL stretched and above historic averages. But yes, there is still quite a bit of growth to be expected from these industries. CAPEX expectations continue to grow for the AI market, hundreds of billions of dollars contributed to new chips, new center, and new leases designed to continue the historical buildout we’ve witnessed with the AI rush.

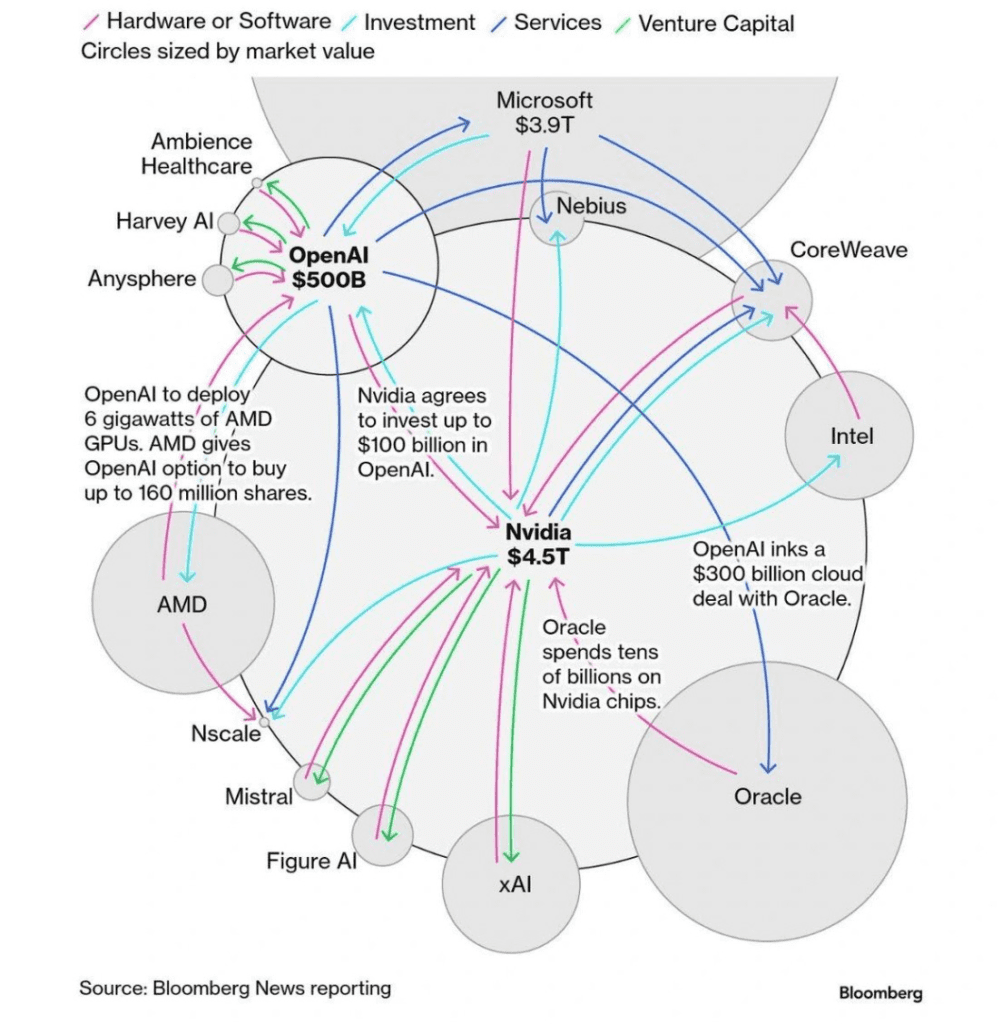

With each new contract, however, it seems that the market hopes for actual execution, which is entirely understandable. OpenAI, the owner of ChatGPT, continues to raise their CAPEX and operating expense projections, without a boost in revenue to boot. The company continues to push back its expected cash-flow positive year, and it seems like there are many, many years and hundreds of billions that the company is expected to spend on a roll-out, without much of a hope for profit.

Companies like Anthropic, the group behind Claude AI, expect sooner profit realization, but still with tens of billions in expenditures expected. There really isn’t much to show for the hundreds of billions being invested, at least without taking a look at the rising water, electricity, and rent prices, and Wall Street (and retail) is hoping to see some change soon.

Despite this though, at a valuation and macroeconomic standpoint, this stock market is at an investment opportunity we haven’t seen in a while. Countless industries and countless companies are being discounted with risks that are less likely to be actualized. Anthropic just showcased their future AI uses within the software industry, and much of what they showed was an extension of current software abilities, not items made to replace.

Is AI a threat to SaaS, jobs, and other markets? Yes. It is overvalued? Yes. Is there a bubble? Yes.

But that doesn’t mean it’s a bad time to invest or a bad time to look around in the market for good opportunities. There are still thousands of companies and thousands of stocks at amazing prices riding this rising AI wave, and there is a lot of money to be made. With the recent weakness in the market, now might be as good of a time as ever.

Don’t let a bubble scare you. We have seen countless bubbles with actual money to be made. These cycles can last for years, if not decades, and it’s very possible we can see it deflate as time comes and goes. Bubbles don’t have to necessarily pop — if you inflate one, it’s entirely possible to slowly drain it the same way.

With valuations very quickly settling at closer to century averages despite historic revenue growth, now might be as good a time as ever to make a move, a small one albeit, into distressed markets. After all, the best time to go shopping is when everybody else is scared.

Of course, this is not investment advice. Do you own due diligence, these are just my opinions and my opinions only.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

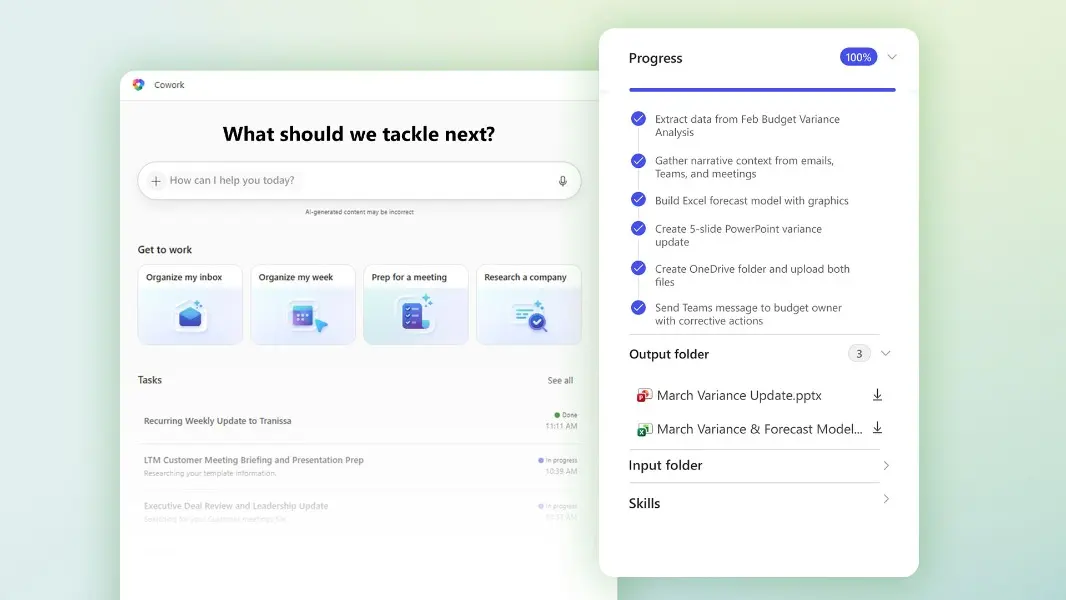

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.

Today’s market is as convoluted as it gets — year to date the S&P 500 is up just 1.46%, essentially the fourth time we’ve reached that mark in just three months. Software stocks have seen their valuations absolutely obliterated, while AI companies have seen their stock prices follow suit. Who knows what each day brings for the market? And that’s without including every single policy change and political interaction that each wild, wild day includes.

Speaking of, that’s how we started off the year, Trump’s tariffs bringing huge swings in stock pricing and market moves. Some days stocks shot up 10%, before getting absolutely obliterated the next day. Policy uncertainty in Washington pushes stocks lower while promises of trillions in tariff revenue boosts markets the next day. Nobody knows just how tariffs might be implemented or impact global trade, and it seems nobody really cares to determine anything concrete or resolute, when we can rely on the chaos of the standard 2026 day.

The good news comes for those that love buying the dip though — this uncertainty has dragged down the valuation of the S&P 500, despite record numbers from the index’s top companies, from 22x price to earnings at the start of the year down to a more manageable 20 times, much more in line with previous and historical figures. While many valuations for individual stocks are inflated (obviously), the overall index and market as a whole have tended to found a much softer landing for valuations. PEG (price to earnings/earnings growth ratio) figures have fallen, with many of the top companies (including the multi-trillion-dollar NVIDIA) having fallen below a 1X ratio, a figure famously touted as suggesting affordability in stocks compared to their earnings potential.

Nonetheless, Wall Street doesn’t seem to be very optimistic about the chances for the market to continue this substantial growth, discounting stocks relative to their recent valuations off worries of slower growth and general tariff headwinds. It seems much of the recent broad market pullback has been because of worries over valuation, meaning that we’re reaching much more affordable positions despite growth that has continued above expectations. While Wall Street keeps cutting growth forecasts for many of the larger, AI-focused corporations, it seems that each company brings a new surprise in quarterly earnings or their projected upcoming reports for the positive.

Despite this cut, much of the disappointment in earnings have actually come from defensive positions. Home improvement stalwarts Lowe’s and Home Depot reported earnings this week, Lowe’s actually beating on both top-line and bottom-line growth (and reporting nearly 10% growth year over year!), before being dragged down on soft growth expectations for the next year. While AI companies and many software corporations have begun to actually re-up their projections for their 2026 reports, many defensive opportunities have seen slower growth or worries about the general environment.

Even with these issues though, defensive positions have held up better than hypergrowth stocks — capital keeps rotating from these riskier investments into small-caps, industries, and the like despite disappointing earnings and concerns over a softer spending market and slowed non-AI GDP growth. Doesn’t seem to impact the money being invested though.

Speaking of AI GDP growth, back to the subject at hand — yes, tech sector valuations are STILL stretched and above historic averages. But yes, there is still quite a bit of growth to be expected from these industries. CAPEX expectations continue to grow for the AI market, hundreds of billions of dollars contributed to new chips, new center, and new leases designed to continue the historical buildout we’ve witnessed with the AI rush.

With each new contract, however, it seems that the market hopes for actual execution, which is entirely understandable. OpenAI, the owner of ChatGPT, continues to raise their CAPEX and operating expense projections, without a boost in revenue to boot. The company continues to push back its expected cash-flow positive year, and it seems like there are many, many years and hundreds of billions that the company is expected to spend on a roll-out, without much of a hope for profit.

Companies like Anthropic, the group behind Claude AI, expect sooner profit realization, but still with tens of billions in expenditures expected. There really isn’t much to show for the hundreds of billions being invested, at least without taking a look at the rising water, electricity, and rent prices, and Wall Street (and retail) is hoping to see some change soon.

Despite this though, at a valuation and macroeconomic standpoint, this stock market is at an investment opportunity we haven’t seen in a while. Countless industries and countless companies are being discounted with risks that are less likely to be actualized. Anthropic just showcased their future AI uses within the software industry, and much of what they showed was an extension of current software abilities, not items made to replace.

Is AI a threat to SaaS, jobs, and other markets? Yes. It is overvalued? Yes. Is there a bubble? Yes.

But that doesn’t mean it’s a bad time to invest or a bad time to look around in the market for good opportunities. There are still thousands of companies and thousands of stocks at amazing prices riding this rising AI wave, and there is a lot of money to be made. With the recent weakness in the market, now might be as good of a time as ever.

Don’t let a bubble scare you. We have seen countless bubbles with actual money to be made. These cycles can last for years, if not decades, and it’s very possible we can see it deflate as time comes and goes. Bubbles don’t have to necessarily pop — if you inflate one, it’s entirely possible to slowly drain it the same way.

With valuations very quickly settling at closer to century averages despite historic revenue growth, now might be as good a time as ever to make a move, a small one albeit, into distressed markets. After all, the best time to go shopping is when everybody else is scared.

Of course, this is not investment advice. Do you own due diligence, these are just my opinions and my opinions only.

Venture funding reached a record-shattering $300 billion in Q1 2026 as investors pivot toward agentic AI and energy infrastructure, marking a new industrial era.

Microsoft is betting that two AI models working together are better than one, and it just shipped the proof.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

SanDisk reports a blowout Q2 2026 with $3.03 billion in revenue and $6.20 EPS. Despite the stock being down today, the future valuation remains massive.