IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

IonQ enters 2026 as the undisputed leader in quantum fidelity, boasting record-breaking 99.99% gate accuracy and a war chest of $3.5 billion to fuel its global expansion.

The transition from classical computing to quantum processing has often been described as the “Holy Grail” of modern technology. For years, the industry was defined by high-concept white papers and lab-bound prototypes that felt decades away from commercial reality. However, as we navigate the opening weeks of 2026, that narrative has fundamentally changed. The speculative fog is lifting: and IonQ is standing at the center of the clearing.

While the broader tech market spent much of 2025 obsessing over generative AI and LLM efficiency, a quiet but profound shift occurred in the quantum sector. IonQ, the Maryland-based pure-play quantum leader, spent the last twelve months executing a masterclass in hardware scaling and strategic consolidation. If 2024 was the year of “what if,” 2025 was the year of “here it is,” and 2026 is shaping up to be the year of “at scale.”

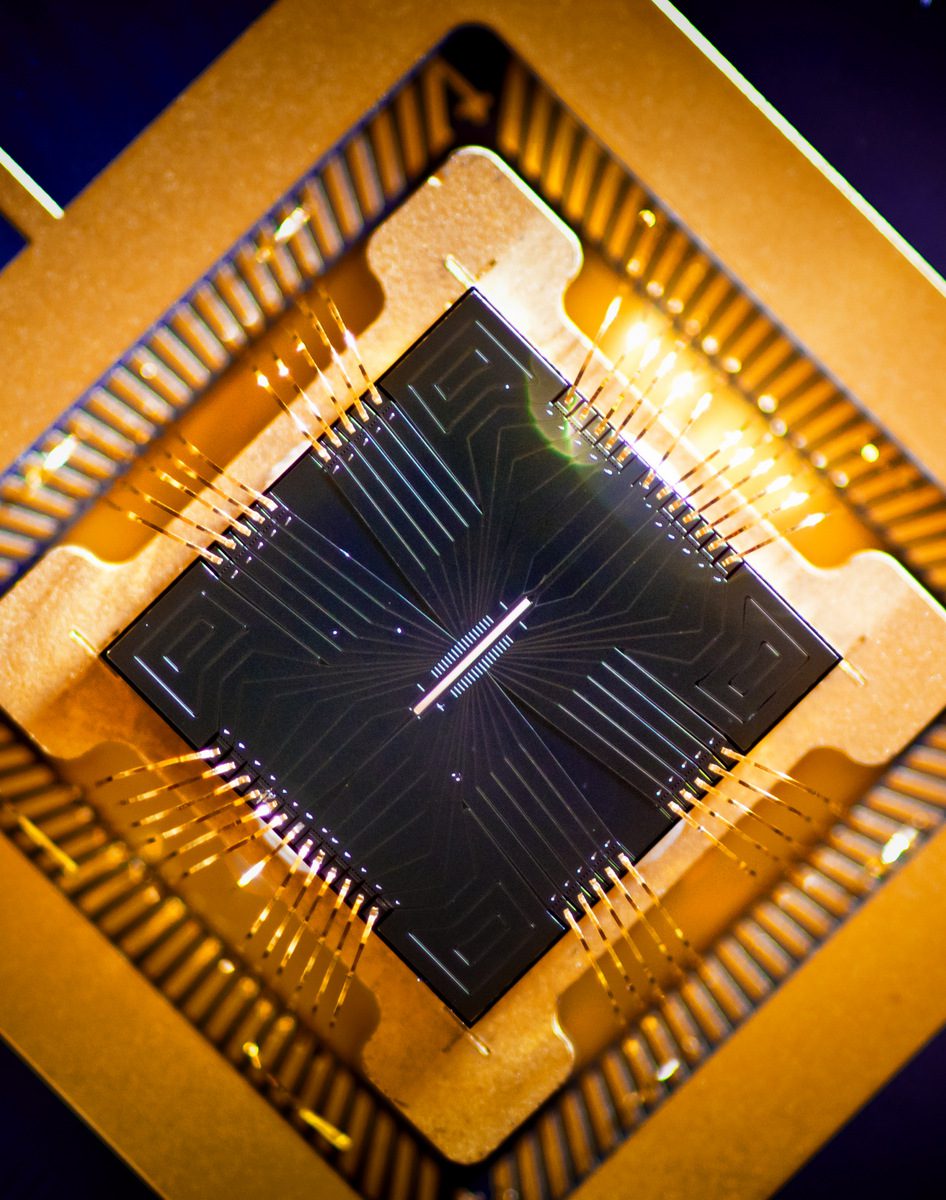

To understand why IonQ is currently outperforming its peers in technical credibility, we have to look at the “four-nines” benchmark. In October 2025, IonQ released technical papers demonstrating 99.99% two-qubit gate performance. This was not just a minor improvement: it was a world record that placed IonQ as the first and only company to cross that specific threshold.

In the world of quantum, fidelity is everything. Most competitors, including those using superconducting circuits like Google or IBM, struggle with “noise” and decoherence. When you are dealing with subatomic particles, even the slightest vibration or temperature fluctuation can ruin a calculation. IonQ’s trapped ion approach uses individual atoms as qubits, which are naturally identical and highly stable. By reaching 99.99% fidelity, the company has effectively solved the hardware reliability problem that has plagued the industry for a decade. This level of accuracy means that error correction, which usually eats up the majority of a quantum computer’s processing power, becomes significantly more efficient.

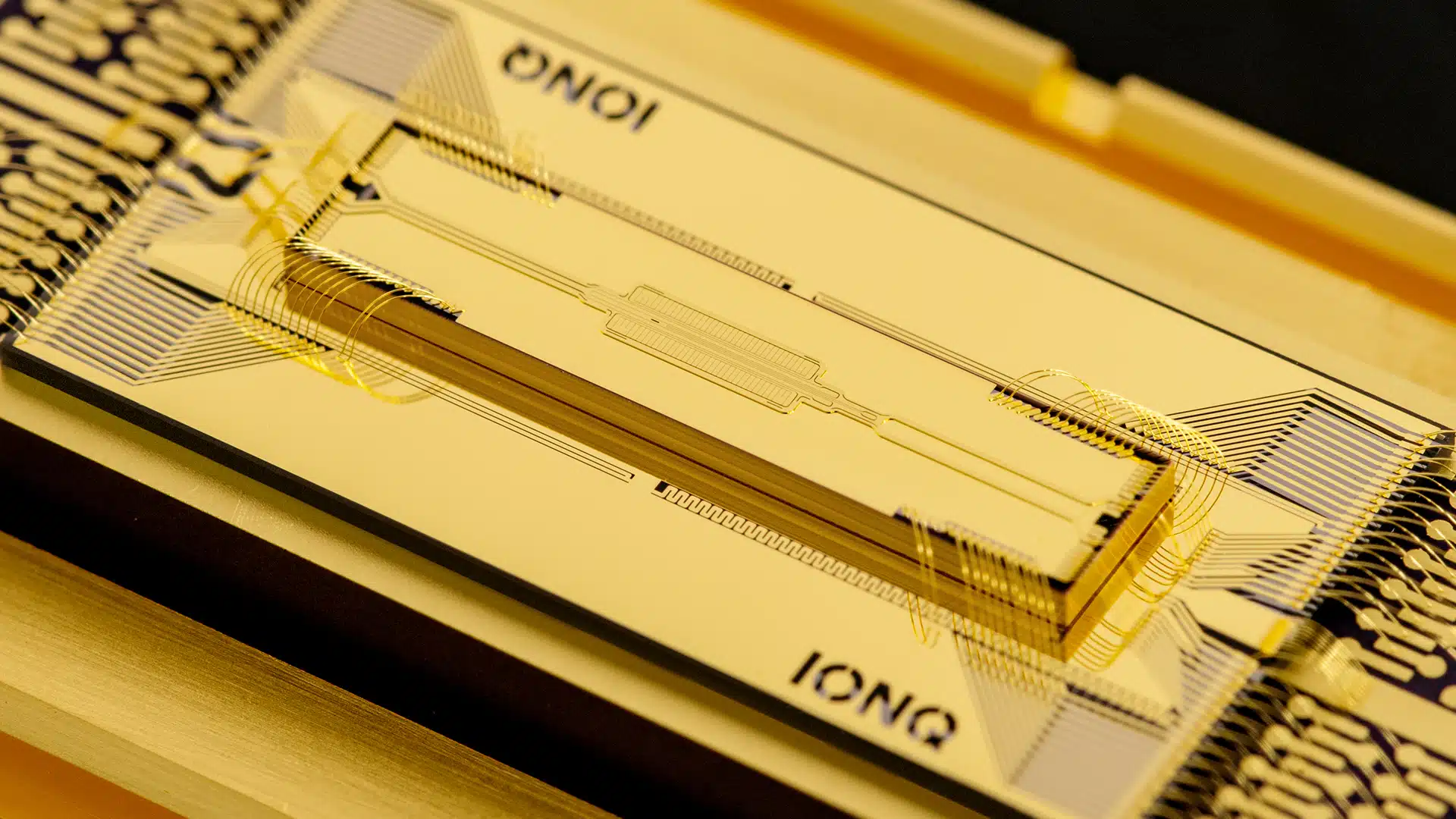

This technical superiority translated directly into the company’s product roadmap. IonQ reached its Algorithmic Qubit (AQ) 64 goal on its Tempo system three months ahead of schedule in late 2025. For an industry where deadlines are often viewed as suggestions, hitting a major milestone early is a massive signal to institutional investors. Tempo is now the benchmark against which all other commercial quantum systems are measured. It is scheduled for wider commercial shipping throughout 2026, providing the first real opportunity for enterprise-scale quantum advantage.

One of the biggest risks for “deep tech” companies is the burn rate. Developing quantum computers is expensive: it requires world-class physicists, custom semiconductor fabrication, and immense research and development budgets. However, IonQ enters 2026 with a financial profile that looks more like an established mid-cap than a struggling startup.

According to recent financial reports, IonQ maintains over $3.5 billion in cash and cash equivalents with effectively no debt. This is a staggering amount of liquidity for a company in this space. It provides IonQ with two critical advantages:

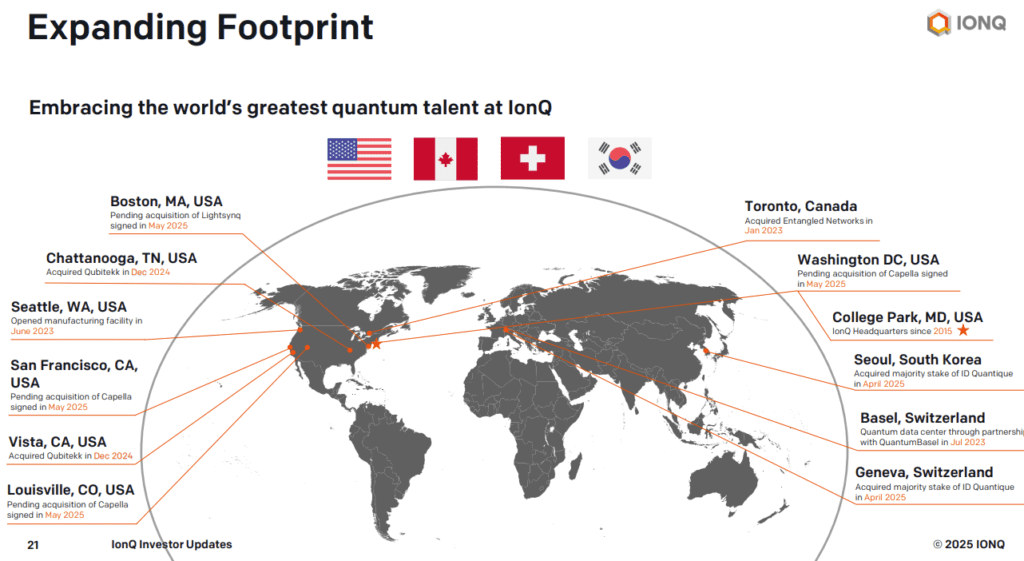

In the latter half of 2025, IonQ completed a series of acquisitions that fundamentally changed the company’s scope. The purchase of Oxford Ionics brought in world-leading 2D ion trap technology, which is expected to increase qubit density by up to 300 times. Then came the acquisition of Skyloom Global, a specialist in optical communications.

This move into networking is crucial. IonQ is no longer just building a “box” that sits in a data center: it is building the “Quantum Internet.” By integrating Skyloom’s space-based optical systems with its existing ground-based networking partnerships, IonQ is positioning itself to be the primary provider of quantum key distribution (QKD). This is the infrastructure that will keep global communications secure in a post-RSA encryption world.

Critics often point to IonQ’s valuation compared to its current revenue, but that view misses the acceleration happening in the order books. In 2024, the company reported roughly $43 million in revenue. For the fiscal year 2025, the company is projected to cross the $110 million mark, representing a doubling of sales for the fourth year in a row.

Looking ahead to 2026, consensus analyst estimates suggest revenue could jump to $200 million or more. This growth is being driven by a shift from research-based “consulting” contracts to high-margin Quantum-as-a-Service (QCaaS) subscriptions.

The list of names currently utilizing IonQ’s hardware reads like a “who’s who” of the Fortune 500:

Furthermore, the company’s global footprint expanded significantly in late 2025. IonQ finalized the delivery of a 100-qubit Tempo system to South Korea’s KISTI and expanded its partnership with Switzerland’s QuantumBasel in a deal worth over $60 million. These are not just research pilots: these are multi-year infrastructure commitments.

The single most important catalyst for IonQ in 2026 is the convergence of quantum computing and artificial intelligence. We have reached a point where classical GPUs are beginning to hit a “diminishing returns” wall when it comes to certain types of AI model fine-tuning.

IonQ’s “Quantum Fine-Tuning” approach adds a quantum layer to classical LLMs. In tests conducted throughout 2025, this hybrid approach allowed models to capture higher-dimensional patterns that classical systems simply missed. As enterprises look for ways to make their AI models “smarter” rather than just “larger,” IonQ’s hardware provides a unique solution.

In January 2026, IonQ made a significant hire that signals its intent to dominate the national security market. Katie Arrington, a veteran of the Department of Defense and a well-known advocate for technology security, joined as the company’s Chief Information Officer. This move suggests that IonQ is preparing for a massive ramp-up in classified government contracts, specifically through its IonQ Federal subsidiary. Arrington’s expertise in supply chain security and government procurement is exactly what the company needs as it transitions from a technology developer to a core utility provider for the US government.

The quantum computing race is often framed as a battle between different “qubit modalities.” On one side, you have superconducting qubits (IBM, Google, Rigetti). On the other, you have trapped ions (IonQ, Quantinuum).

As we sit here in 2026, the advantages of the trapped ion approach have become undeniable for commercial applications. Superconducting systems require massive dilution refrigerators to keep qubits near absolute zero, making them difficult to scale and maintain. IonQ’s systems, by contrast, operate at more manageable temperatures and can be housed in standard server racks.

Rigetti Computing, once a major rival, has struggled to keep pace. While IonQ was selected for Stage B of the major DARPA quantum benchmarking initiative in 2025, Rigetti was notably absent from that group. This divergence in government validation is a clear indicator of which technology is currently winning the “utility” argument.

Investing in IonQ in 2026 requires a shift in perspective. You are not buying a “computer manufacturer” in the traditional sense. You are buying a stake in the operating system of the 21st century.

The stock has seen some volatility recently: dropping roughly 40% from its October 2025 highs due to profit-taking and general macro concerns. For the long-term investor, this looks like a classic “buying the dip” opportunity. With a 2026 price-to-sales ratio that is starting to look more reasonable given the triple-digit revenue growth, IonQ is no longer just a speculative science project. It is an essential pillar of the modern technology portfolio.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.

SanDisk reports a blowout Q2 2026 with $3.03 billion in revenue and $6.20 EPS. Despite the stock being down today, the future valuation remains massive.

IonQ enters 2026 as the undisputed leader in quantum fidelity, boasting record-breaking 99.99% gate accuracy and a war chest of $3.5 billion to fuel its global expansion.

The transition from classical computing to quantum processing has often been described as the “Holy Grail” of modern technology. For years, the industry was defined by high-concept white papers and lab-bound prototypes that felt decades away from commercial reality. However, as we navigate the opening weeks of 2026, that narrative has fundamentally changed. The speculative fog is lifting: and IonQ is standing at the center of the clearing.

While the broader tech market spent much of 2025 obsessing over generative AI and LLM efficiency, a quiet but profound shift occurred in the quantum sector. IonQ, the Maryland-based pure-play quantum leader, spent the last twelve months executing a masterclass in hardware scaling and strategic consolidation. If 2024 was the year of “what if,” 2025 was the year of “here it is,” and 2026 is shaping up to be the year of “at scale.”

To understand why IonQ is currently outperforming its peers in technical credibility, we have to look at the “four-nines” benchmark. In October 2025, IonQ released technical papers demonstrating 99.99% two-qubit gate performance. This was not just a minor improvement: it was a world record that placed IonQ as the first and only company to cross that specific threshold.

In the world of quantum, fidelity is everything. Most competitors, including those using superconducting circuits like Google or IBM, struggle with “noise” and decoherence. When you are dealing with subatomic particles, even the slightest vibration or temperature fluctuation can ruin a calculation. IonQ’s trapped ion approach uses individual atoms as qubits, which are naturally identical and highly stable. By reaching 99.99% fidelity, the company has effectively solved the hardware reliability problem that has plagued the industry for a decade. This level of accuracy means that error correction, which usually eats up the majority of a quantum computer’s processing power, becomes significantly more efficient.

This technical superiority translated directly into the company’s product roadmap. IonQ reached its Algorithmic Qubit (AQ) 64 goal on its Tempo system three months ahead of schedule in late 2025. For an industry where deadlines are often viewed as suggestions, hitting a major milestone early is a massive signal to institutional investors. Tempo is now the benchmark against which all other commercial quantum systems are measured. It is scheduled for wider commercial shipping throughout 2026, providing the first real opportunity for enterprise-scale quantum advantage.

One of the biggest risks for “deep tech” companies is the burn rate. Developing quantum computers is expensive: it requires world-class physicists, custom semiconductor fabrication, and immense research and development budgets. However, IonQ enters 2026 with a financial profile that looks more like an established mid-cap than a struggling startup.

According to recent financial reports, IonQ maintains over $3.5 billion in cash and cash equivalents with effectively no debt. This is a staggering amount of liquidity for a company in this space. It provides IonQ with two critical advantages:

In the latter half of 2025, IonQ completed a series of acquisitions that fundamentally changed the company’s scope. The purchase of Oxford Ionics brought in world-leading 2D ion trap technology, which is expected to increase qubit density by up to 300 times. Then came the acquisition of Skyloom Global, a specialist in optical communications.

This move into networking is crucial. IonQ is no longer just building a “box” that sits in a data center: it is building the “Quantum Internet.” By integrating Skyloom’s space-based optical systems with its existing ground-based networking partnerships, IonQ is positioning itself to be the primary provider of quantum key distribution (QKD). This is the infrastructure that will keep global communications secure in a post-RSA encryption world.

Critics often point to IonQ’s valuation compared to its current revenue, but that view misses the acceleration happening in the order books. In 2024, the company reported roughly $43 million in revenue. For the fiscal year 2025, the company is projected to cross the $110 million mark, representing a doubling of sales for the fourth year in a row.

Looking ahead to 2026, consensus analyst estimates suggest revenue could jump to $200 million or more. This growth is being driven by a shift from research-based “consulting” contracts to high-margin Quantum-as-a-Service (QCaaS) subscriptions.

The list of names currently utilizing IonQ’s hardware reads like a “who’s who” of the Fortune 500:

Furthermore, the company’s global footprint expanded significantly in late 2025. IonQ finalized the delivery of a 100-qubit Tempo system to South Korea’s KISTI and expanded its partnership with Switzerland’s QuantumBasel in a deal worth over $60 million. These are not just research pilots: these are multi-year infrastructure commitments.

The single most important catalyst for IonQ in 2026 is the convergence of quantum computing and artificial intelligence. We have reached a point where classical GPUs are beginning to hit a “diminishing returns” wall when it comes to certain types of AI model fine-tuning.

IonQ’s “Quantum Fine-Tuning” approach adds a quantum layer to classical LLMs. In tests conducted throughout 2025, this hybrid approach allowed models to capture higher-dimensional patterns that classical systems simply missed. As enterprises look for ways to make their AI models “smarter” rather than just “larger,” IonQ’s hardware provides a unique solution.

In January 2026, IonQ made a significant hire that signals its intent to dominate the national security market. Katie Arrington, a veteran of the Department of Defense and a well-known advocate for technology security, joined as the company’s Chief Information Officer. This move suggests that IonQ is preparing for a massive ramp-up in classified government contracts, specifically through its IonQ Federal subsidiary. Arrington’s expertise in supply chain security and government procurement is exactly what the company needs as it transitions from a technology developer to a core utility provider for the US government.

The quantum computing race is often framed as a battle between different “qubit modalities.” On one side, you have superconducting qubits (IBM, Google, Rigetti). On the other, you have trapped ions (IonQ, Quantinuum).

As we sit here in 2026, the advantages of the trapped ion approach have become undeniable for commercial applications. Superconducting systems require massive dilution refrigerators to keep qubits near absolute zero, making them difficult to scale and maintain. IonQ’s systems, by contrast, operate at more manageable temperatures and can be housed in standard server racks.

Rigetti Computing, once a major rival, has struggled to keep pace. While IonQ was selected for Stage B of the major DARPA quantum benchmarking initiative in 2025, Rigetti was notably absent from that group. This divergence in government validation is a clear indicator of which technology is currently winning the “utility” argument.

Investing in IonQ in 2026 requires a shift in perspective. You are not buying a “computer manufacturer” in the traditional sense. You are buying a stake in the operating system of the 21st century.

The stock has seen some volatility recently: dropping roughly 40% from its October 2025 highs due to profit-taking and general macro concerns. For the long-term investor, this looks like a classic “buying the dip” opportunity. With a 2026 price-to-sales ratio that is starting to look more reasonable given the triple-digit revenue growth, IonQ is no longer just a speculative science project. It is an essential pillar of the modern technology portfolio.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.

SanDisk reports a blowout Q2 2026 with $3.03 billion in revenue and $6.20 EPS. Despite the stock being down today, the future valuation remains massive.

Celestica’s record-shattering Q4 2025 results showcase a massive leap in adjusted operating margins to 7.7%, driven by surging demand for AI data center technologies.