Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

The date is February 25, 2026, and the quantum computing industry just had its “Netscape moment.” For years, the bears in the financial community have dismissed quantum as a “decade-away” technology: a science project that lived in ivory towers and expensive labs but lacked the grit of a real business. Today, IonQ (NYSE: IONQ) effectively ended that debate. When the company reported its fourth-quarter and full-year 2025 results, it didn’t just beat guidance: it redefined the scale of what is possible in this nascent sector.

IonQ has become the first public quantum company in history to report more than $100 million in annual GAAP revenue. While that might sound like small change compared to the trillion-dollar hyperscalers, the context is everything. We are witnessing the birth of a new infrastructure layer, and IonQ is positioning itself not just as a manufacturer of computers, but as the merchant supplier for the entire Western quantum ecosystem.

The most striking data point from the 2025 report isn’t the total revenue, but the mix of who is paying for it. Over 60 percent of IonQ’s revenue now comes from commercial customers. This is a massive departure from the early days when revenue was almost entirely driven by government research grants. It tells us that enterprises in pharmaceuticals, finance, and logistics are no longer just “exploring” quantum: they are integrating it into their production roadmaps.

The fourth quarter was particularly explosive. IonQ recognized $61.9 million in revenue, which represents a 429 percent increase over the same period in 2024. For the full year, the company brought in $130.0 million, representing 202 percent year-over-year growth. For an analyst, these aren’t just growth numbers: they are proof of a “land and expand” strategy that is working. When repeat buyers comprise a significant portion of your pipeline, it indicates that the technology is delivering a tangible return on investment.

One of the biggest concerns for investors in deep-tech sectors is the “burn rate.” Developing quantum hardware is expensive. It requires specialized physicists, proprietary materials, and massive R&D budgets. However, IonQ has insulated itself from the volatility of capital markets. The company ended 2025 with $3.3 billion in cash, cash equivalents, and investments.

This liquidity is not just a safety net: it is a weapon. It allows IonQ to fund its roadmap without the constant threat of dilutive secondary offerings. More importantly, it enabled the recent $1.8 billion acquisition of SkyWater Technology. By using its balance sheet to buy a trusted U.S. foundry, IonQ has secured its own supply chain and effectively “moated” its production capability against geopolitical instability.

The merger with SkyWater Technology is the defining strategic event of this cycle. By acquiring the largest exclusively U.S.-based pure-play semiconductor foundry, IonQ has transitioned into a vertically integrated powerhouse. This isn’t just about making chips: it is about owning the “Trusted Fab” that the U.S. government and its allies require for mission-critical applications.

In a world of increasing decoupling between Western and Eastern tech stacks, “sovereign compute” has become the primary requirement for defense and national security. The SkyWater deal provides IonQ with DMEA Category 1A Trusted accreditation. This means IonQ can now provide end-to-end design, prototyping, manufacturing, and packaging within a secure U.S. infrastructure.

This move supports the newly launched IonQ Federal division, which is already seeing massive traction. In early 2026, the company was selected by DARPA for Phase B of the Quantum Benchmarking Initiative (QBI). This isn’t just a research contract: it is a validator of IonQ’s ability to hit the “fault-tolerant” milestones that will lead to real-world utility. When the Department of War looks for a quantum partner, they aren’t looking for the most interesting academic paper: they are looking for the most reliable domestic supply chain.

Under the leadership of Niccolo de Masi, IonQ is executing a “merchant supplier” model. They are becoming the infrastructure that other companies build upon. With the SkyWater assets, IonQ will continue to serve as a pure-play foundry for the entire industry. This creates a fascinating revenue stream: they will be making money even when their competitors succeed, by providing the specialized silicon photonics and superconducting integrated circuits that the broader industry needs.

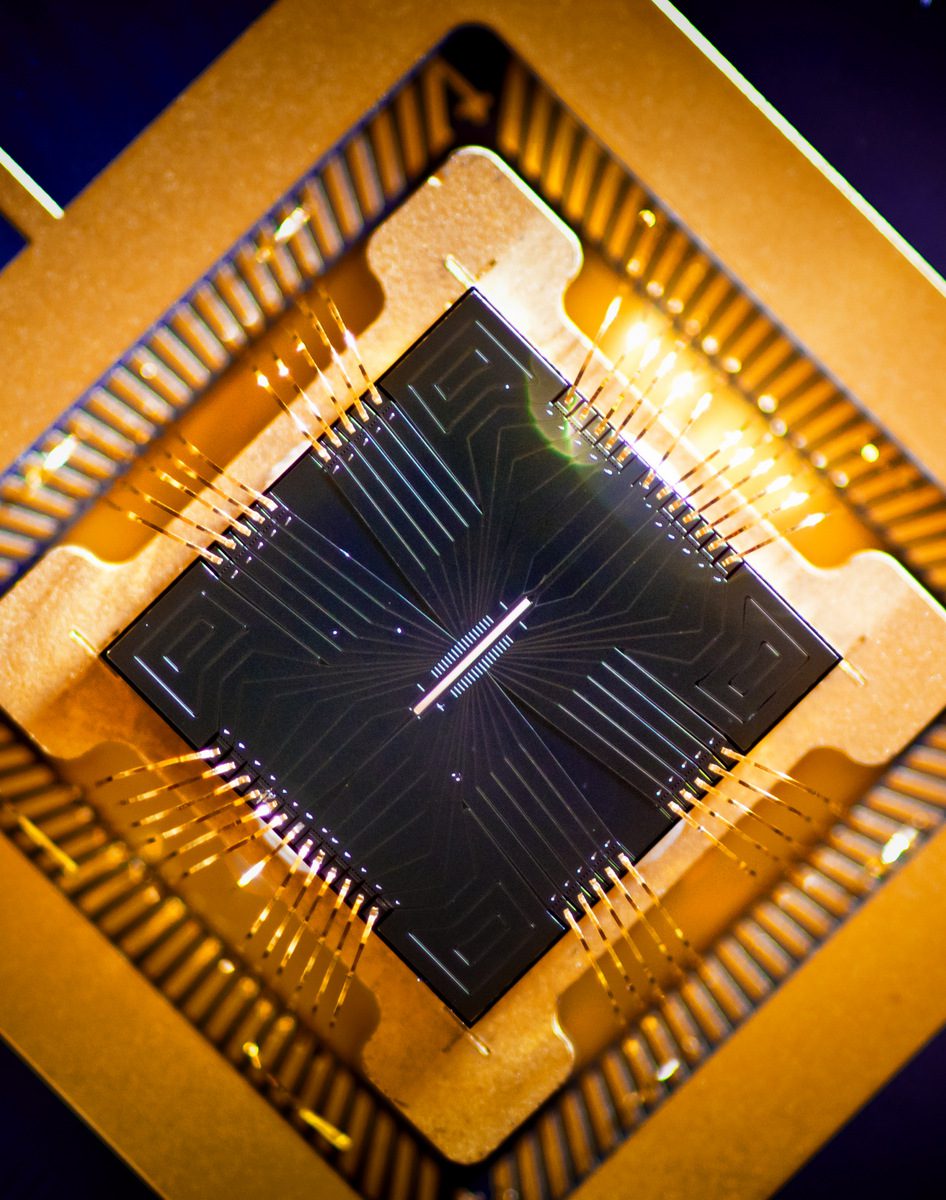

The hardware roadmap remains the core of the thesis. In 2025, IonQ achieved a world-record 99.99 percent two-qubit gate fidelity. This is the “magic number” required for efficient error correction. Without this level of precision, scaling a quantum computer is like building a skyscraper on a foundation of sand: eventually, the noise overwhelms the signal.

The sale of a fifth-generation, 100-qubit system to the Korea Institute of Science and Technology Information (KISTI) is a major commercial win. This system will be at the heart of South Korea’s largest quantum-classical compute platform. By integrating with NVIDIA acceleration and high-performance computing (HPC) environments, IonQ is proving that quantum computers don’t live in a vacuum. They are co-processors that will work alongside classical GPUs to solve the world’s most complex problems.

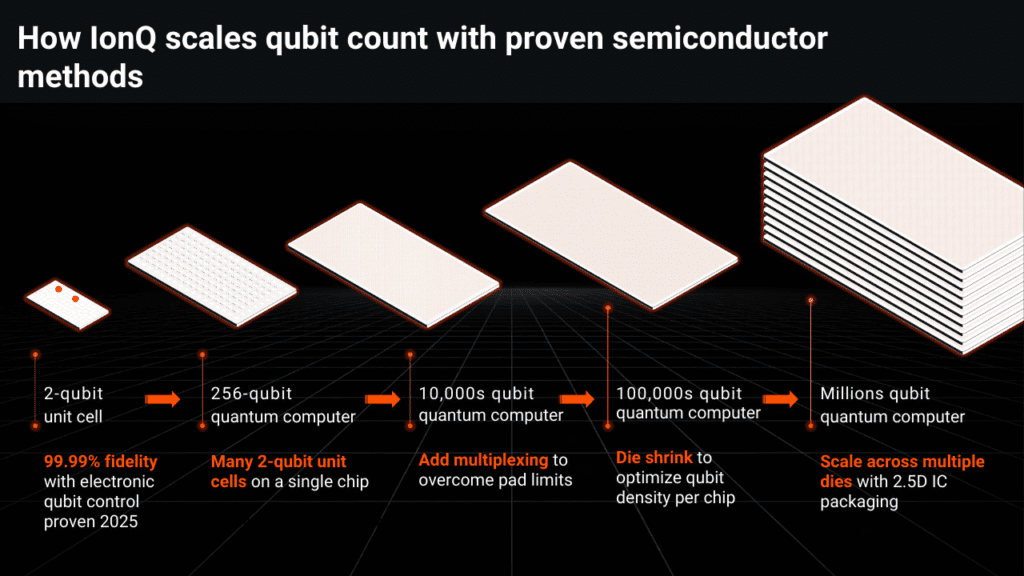

The accelerated roadmap is perhaps the most ambitious part of the 2025 reporting. With the embedded access to SkyWater’s foundry, IonQ expects to begin functional testing of its 200,000 qubit QPUs in 2028. These units will enable over 8,000 ultra-high fidelity logical qubits. For context, this is the scale at which quantum computers begin to fundamentally disrupt the pharmaceutical industry by simulating molecular interactions that are currently impossible to model on classical supercomputers.

IonQ is no longer just a “compute” company. They have expanded their platform into four distinct domains that create a multi-layered revenue model.

This “Land, Sea, Air, and Space” strategy provides diversification. If the compute market hits a temporary plateau, the sensing and networking markets provide a stable floor. It is a full-stack approach that mirrors the early days of companies like Cisco or IBM, where the hardware and the network are inseparable.

The guidance for 2026 is equally aggressive. IonQ expects revenue to land between $225 million and $245 million. At the midpoint, this represents nearly 85 percent growth on an organic basis.

Investors looking at the headline GAAP net income for Q4 might see a staggering $753.7 million and think the company is already printing money. It is important to look at the fine print: that number was primarily driven by a $949.6 million non-cash gain on the change in fair value of warrant liabilities.

On an adjusted basis, which is how management actually runs the business, IonQ reported an Adjusted EBITDA loss of $67.4 million for the quarter. This is expected. The company is in a heavy investment phase. In 2025, R&D spend increased by 123 percent year-over-year. Management is making the correct long-term call: they are spending now to capture the dominant market share of the next decade.

The recent hires in Q4 and early 2026 speak to the company’s focus on enterprise and government scale. Bringing in Katie Arrington as Chief Information Officer (formerly with the U.S. Department of War) and Scott Millard as Chief Business Officer (formerly with Dell) signals a shift toward professionalized, large-scale sales and security. These aren’t “startup” hires: these are “Fortune 500” hires.

No investment thesis is without risk. For IonQ, the challenges are largely operational and technical.

IonQ has successfully navigated the most difficult phase of its life cycle. It has moved beyond the “proof of concept” stage and into the “commercial infrastructure” stage. By Crossing the $100 million revenue threshold, the company has proven that there is a real, paying market for quantum compute today.

The investment thesis rests on three pillars:

For the long-term investor, the recent quarterly results are a clear signal. IonQ is building the foundational technology of the next fifty years. While the stock will certainly face volatility as the market digests the non-cash warrant adjustments and the long-term R&D burn, the underlying growth trajectory is undeniable. We are no longer asking if quantum will happen: we are now simply measuring how fast IonQ can scale it.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.

SanDisk reports a blowout Q2 2026 with $3.03 billion in revenue and $6.20 EPS. Despite the stock being down today, the future valuation remains massive.

Celestica’s record-shattering Q4 2025 results showcase a massive leap in adjusted operating margins to 7.7%, driven by surging demand for AI data center technologies.

IonQ just shattered the $100 million revenue ceiling, proving that quantum computing is no longer a science experiment but a massive commercial reality for 2026.

The date is February 25, 2026, and the quantum computing industry just had its “Netscape moment.” For years, the bears in the financial community have dismissed quantum as a “decade-away” technology: a science project that lived in ivory towers and expensive labs but lacked the grit of a real business. Today, IonQ (NYSE: IONQ) effectively ended that debate. When the company reported its fourth-quarter and full-year 2025 results, it didn’t just beat guidance: it redefined the scale of what is possible in this nascent sector.

IonQ has become the first public quantum company in history to report more than $100 million in annual GAAP revenue. While that might sound like small change compared to the trillion-dollar hyperscalers, the context is everything. We are witnessing the birth of a new infrastructure layer, and IonQ is positioning itself not just as a manufacturer of computers, but as the merchant supplier for the entire Western quantum ecosystem.

The most striking data point from the 2025 report isn’t the total revenue, but the mix of who is paying for it. Over 60 percent of IonQ’s revenue now comes from commercial customers. This is a massive departure from the early days when revenue was almost entirely driven by government research grants. It tells us that enterprises in pharmaceuticals, finance, and logistics are no longer just “exploring” quantum: they are integrating it into their production roadmaps.

The fourth quarter was particularly explosive. IonQ recognized $61.9 million in revenue, which represents a 429 percent increase over the same period in 2024. For the full year, the company brought in $130.0 million, representing 202 percent year-over-year growth. For an analyst, these aren’t just growth numbers: they are proof of a “land and expand” strategy that is working. When repeat buyers comprise a significant portion of your pipeline, it indicates that the technology is delivering a tangible return on investment.

One of the biggest concerns for investors in deep-tech sectors is the “burn rate.” Developing quantum hardware is expensive. It requires specialized physicists, proprietary materials, and massive R&D budgets. However, IonQ has insulated itself from the volatility of capital markets. The company ended 2025 with $3.3 billion in cash, cash equivalents, and investments.

This liquidity is not just a safety net: it is a weapon. It allows IonQ to fund its roadmap without the constant threat of dilutive secondary offerings. More importantly, it enabled the recent $1.8 billion acquisition of SkyWater Technology. By using its balance sheet to buy a trusted U.S. foundry, IonQ has secured its own supply chain and effectively “moated” its production capability against geopolitical instability.

The merger with SkyWater Technology is the defining strategic event of this cycle. By acquiring the largest exclusively U.S.-based pure-play semiconductor foundry, IonQ has transitioned into a vertically integrated powerhouse. This isn’t just about making chips: it is about owning the “Trusted Fab” that the U.S. government and its allies require for mission-critical applications.

In a world of increasing decoupling between Western and Eastern tech stacks, “sovereign compute” has become the primary requirement for defense and national security. The SkyWater deal provides IonQ with DMEA Category 1A Trusted accreditation. This means IonQ can now provide end-to-end design, prototyping, manufacturing, and packaging within a secure U.S. infrastructure.

This move supports the newly launched IonQ Federal division, which is already seeing massive traction. In early 2026, the company was selected by DARPA for Phase B of the Quantum Benchmarking Initiative (QBI). This isn’t just a research contract: it is a validator of IonQ’s ability to hit the “fault-tolerant” milestones that will lead to real-world utility. When the Department of War looks for a quantum partner, they aren’t looking for the most interesting academic paper: they are looking for the most reliable domestic supply chain.

Under the leadership of Niccolo de Masi, IonQ is executing a “merchant supplier” model. They are becoming the infrastructure that other companies build upon. With the SkyWater assets, IonQ will continue to serve as a pure-play foundry for the entire industry. This creates a fascinating revenue stream: they will be making money even when their competitors succeed, by providing the specialized silicon photonics and superconducting integrated circuits that the broader industry needs.

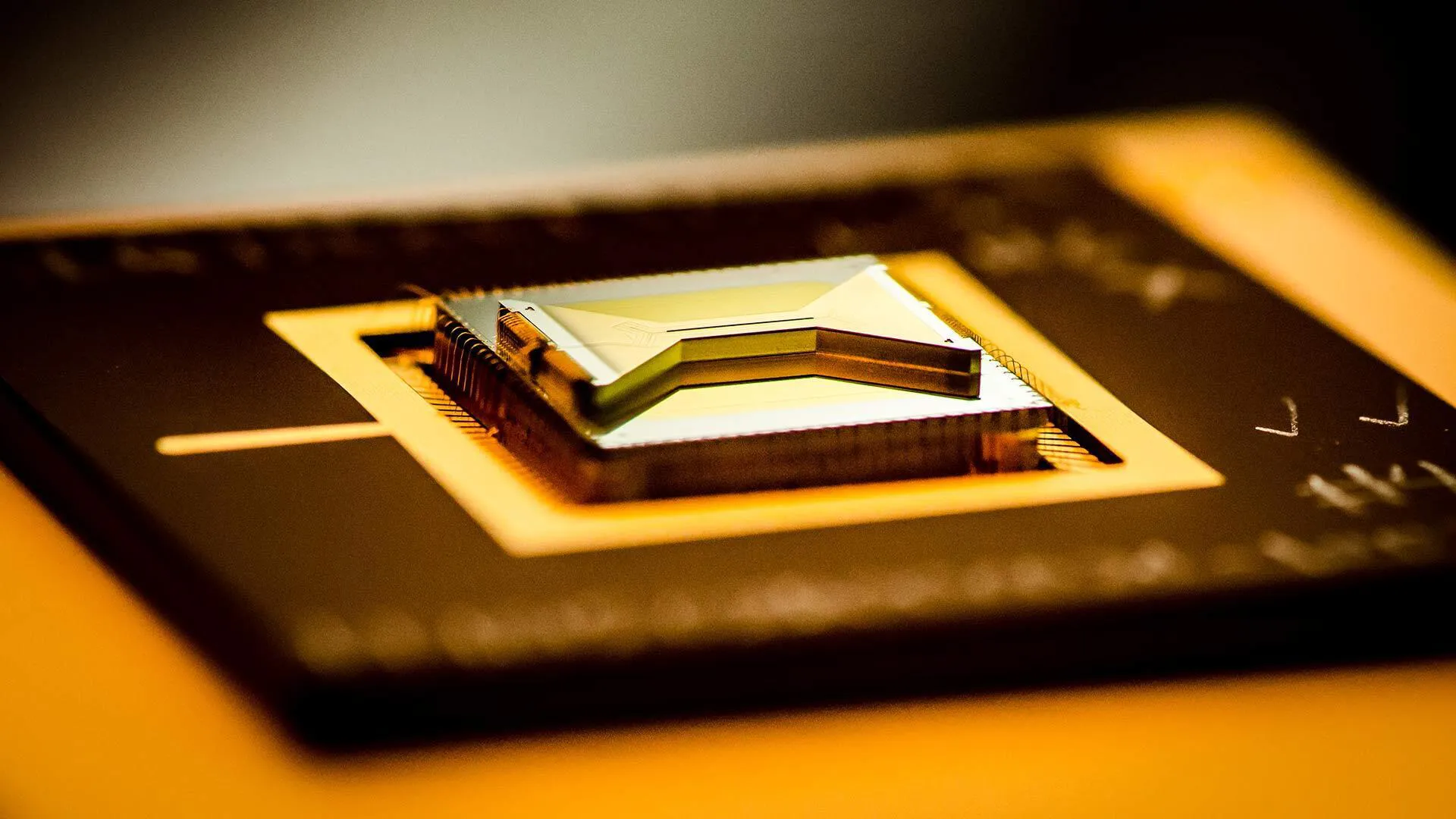

The hardware roadmap remains the core of the thesis. In 2025, IonQ achieved a world-record 99.99 percent two-qubit gate fidelity. This is the “magic number” required for efficient error correction. Without this level of precision, scaling a quantum computer is like building a skyscraper on a foundation of sand: eventually, the noise overwhelms the signal.

The sale of a fifth-generation, 100-qubit system to the Korea Institute of Science and Technology Information (KISTI) is a major commercial win. This system will be at the heart of South Korea’s largest quantum-classical compute platform. By integrating with NVIDIA acceleration and high-performance computing (HPC) environments, IonQ is proving that quantum computers don’t live in a vacuum. They are co-processors that will work alongside classical GPUs to solve the world’s most complex problems.

The accelerated roadmap is perhaps the most ambitious part of the 2025 reporting. With the embedded access to SkyWater’s foundry, IonQ expects to begin functional testing of its 200,000 qubit QPUs in 2028. These units will enable over 8,000 ultra-high fidelity logical qubits. For context, this is the scale at which quantum computers begin to fundamentally disrupt the pharmaceutical industry by simulating molecular interactions that are currently impossible to model on classical supercomputers.

IonQ is no longer just a “compute” company. They have expanded their platform into four distinct domains that create a multi-layered revenue model.

This “Land, Sea, Air, and Space” strategy provides diversification. If the compute market hits a temporary plateau, the sensing and networking markets provide a stable floor. It is a full-stack approach that mirrors the early days of companies like Cisco or IBM, where the hardware and the network are inseparable.

The guidance for 2026 is equally aggressive. IonQ expects revenue to land between $225 million and $245 million. At the midpoint, this represents nearly 85 percent growth on an organic basis.

Investors looking at the headline GAAP net income for Q4 might see a staggering $753.7 million and think the company is already printing money. It is important to look at the fine print: that number was primarily driven by a $949.6 million non-cash gain on the change in fair value of warrant liabilities.

On an adjusted basis, which is how management actually runs the business, IonQ reported an Adjusted EBITDA loss of $67.4 million for the quarter. This is expected. The company is in a heavy investment phase. In 2025, R&D spend increased by 123 percent year-over-year. Management is making the correct long-term call: they are spending now to capture the dominant market share of the next decade.

The recent hires in Q4 and early 2026 speak to the company’s focus on enterprise and government scale. Bringing in Katie Arrington as Chief Information Officer (formerly with the U.S. Department of War) and Scott Millard as Chief Business Officer (formerly with Dell) signals a shift toward professionalized, large-scale sales and security. These aren’t “startup” hires: these are “Fortune 500” hires.

No investment thesis is without risk. For IonQ, the challenges are largely operational and technical.

IonQ has successfully navigated the most difficult phase of its life cycle. It has moved beyond the “proof of concept” stage and into the “commercial infrastructure” stage. By Crossing the $100 million revenue threshold, the company has proven that there is a real, paying market for quantum compute today.

The investment thesis rests on three pillars:

For the long-term investor, the recent quarterly results are a clear signal. IonQ is building the foundational technology of the next fifty years. While the stock will certainly face volatility as the market digests the non-cash warrant adjustments and the long-term R&D burn, the underlying growth trajectory is undeniable. We are no longer asking if quantum will happen: we are now simply measuring how fast IonQ can scale it.

Tariff chaos and an AI reality check are crushing tech valuations. Discover why 2026’s market whiplash is actually a prime contrarian buying opportunity.

SanDisk reports a blowout Q2 2026 with $3.03 billion in revenue and $6.20 EPS. Despite the stock being down today, the future valuation remains massive.

Celestica’s record-shattering Q4 2025 results showcase a massive leap in adjusted operating margins to 7.7%, driven by surging demand for AI data center technologies.

IonQ’s $1.8 billion acquisition of SkyWater transforms its fiscal profile, adding $600 million in projected revenue and shifting valuation toward a vertically integrated model.